Retirement planning, financing and execution is complicated. There is the seemingly simple but nonetheless elusive matter of recognizing the need, allocating the time, and collecting the relevant information. There is the challenge of creating and projecting personal or family financial statements, anticipating retirement dates, and adjusting future funds for inflation and the time value of money. There are somewhat measurable risks, such as market fluctuations during our future retirement years, unanticipated uncertainties, such as global spread of the coronavirus, and that most significant of unknowns, our longevity. Complicated, not impossible.

Perhaps it can help to compare the process to something with which you likely are familiar. I don’t anticipate many readers will actually own a professional sports team, but it seems likely many follow a favorite team or two, or at least can imagine the challenge of team ownership. While there may be many goals, including a quest for community service, personal stature, public recognition, or private satisfaction, many owners have a goal of making money — and winning usually correlates highly with profitability and increased franchise value. Just as you have limited resources to allocate and fund your retirement, a team owner is constrained in hiring talented players — often by a league-imposed salary cap rather than personal resources.

A Parallel Universe

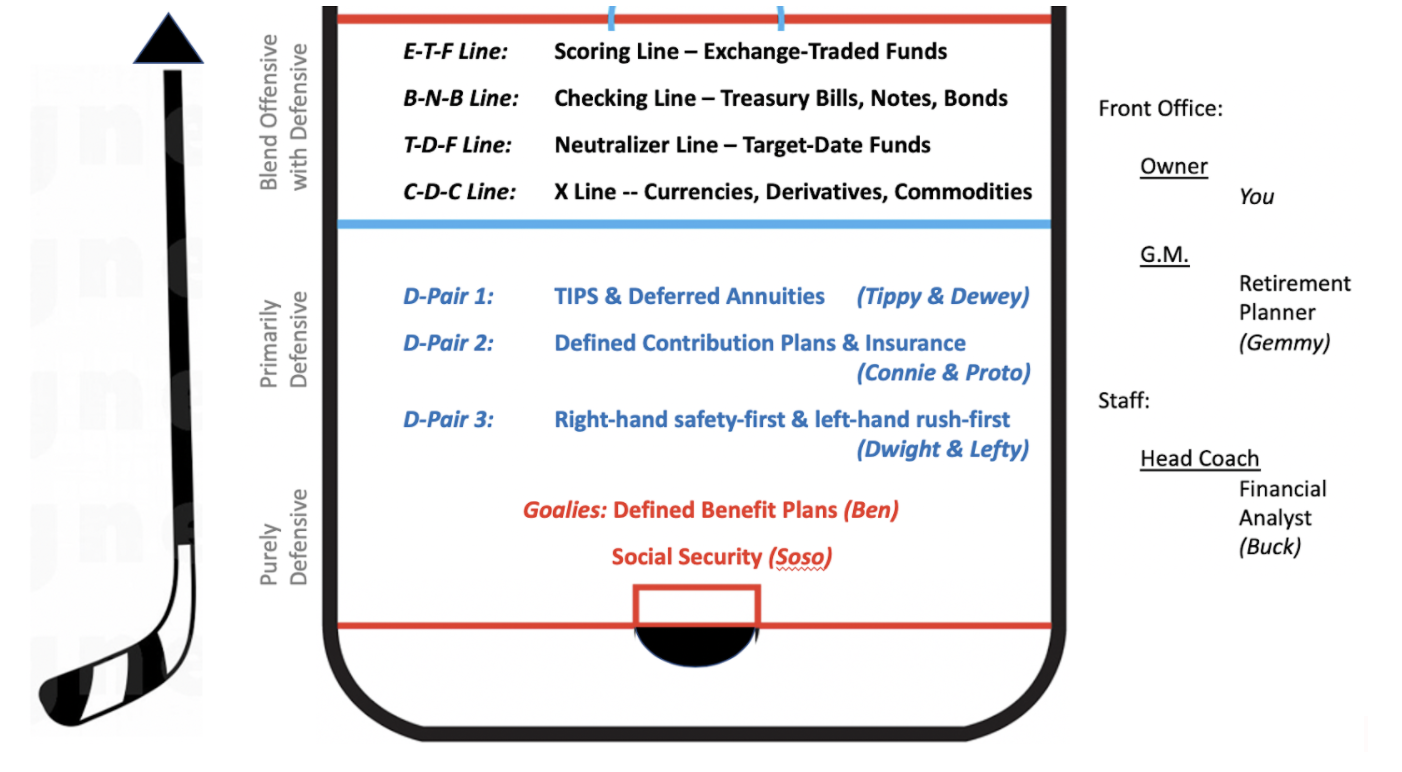

Let’s consider an example. Table 1 creates a blended hockey / retirement team, to highlight similarities in plans.. This hockey team has eight players who focus on defense to minimize scoring lby the other team; a retirement plan could have a similar array of funding sources that support retirement needs, so should have minimal risk exposure. This team then has 12 other players who focus on creating offense to outscore the other team; a retirement plan could have a similar array of more aggressive investments that conceivably could fund retirement wants.

TABLE 1: Envisioning A Blended (Hockey / Retirement) Team

- 2 Goalies

- Soso On loan from another league: (SSA) Social Security Administration

- Ben On loan from another league: (DBP) Defined Benefit Program

- 6 Defensemen

- Tippy Top-D Pairing: A Treasury Inflation-Protected Security

- Dewey Top-D Pairing: A Deferred Annuity

- Connie A mercurial role player, often from a Defined Contribution Program

- Proto Insurance Protection: versatile, covering long-term care, longevity,…

- Dwight Right-Dman: a conservative, a defensive d-man; safety-first

- Lefty Left-Dman: a liberal, offensive d-man; likes to join or lead the rush

- 4 Forward Lines

- E-T-F Line Top Line: Ed-Ted-Fred; a well-synchronized Exchange-Traded Fund

- B-N-B Line Checking Line: Bill-Note-Bond; neutralize top risks from opposition

- T-D-F Line Target-Date-Fund Line: become more conservative later in season

- C-D-C Line Wildcard Line: Commodities-Derivatives-Currencies; limited icetime

- Coaches

- Buck Head Coach = Financial Advisor; selects players, manages games

- Crunch Assistant Coaches: track player performances with data metrics

- Front Office

- Gem General Manager = Retirement Manager; aligns team with its Owner

- Sir Owner: ultimate responsibility for team success; must live with result

Table 2 identifies the goal, constraint, issues and guidelines for these parallel universes.

TABLE 2: Building A Blended (Hockey / Retirement) Team

OBJECTIVE:

- Build a winning team, from General Manager down to the last player

CONSTRAINT:

- For the NHL, a team has a salary cap, as well as salary maximum and minimum

- Unlike the NHL, each “Retirement Team” has an owner-specific salary cap

ISSUES:

- With a salary cap in place; how to allocate limited funds among the 20 players?

- Do I have the right General Manager and Head Coach? Are they overpaid?

- What if Congress and/or your state “pull your goalie”?

- When should you deploy “special teams”, such as a “power play” or “penalty kill”?

GUIDELINES:

- As a hockey owner, you know that goals are the name of the game

- Stable organizations that have a clear plan and stick with it tend to become winners

- No one player can win a championship by himself.

- Winners never quit, and quitters never win.

- There is no elevator to the Stanley Cup; take the stairs.

- Offense creates a headline, but defense creates a champion.

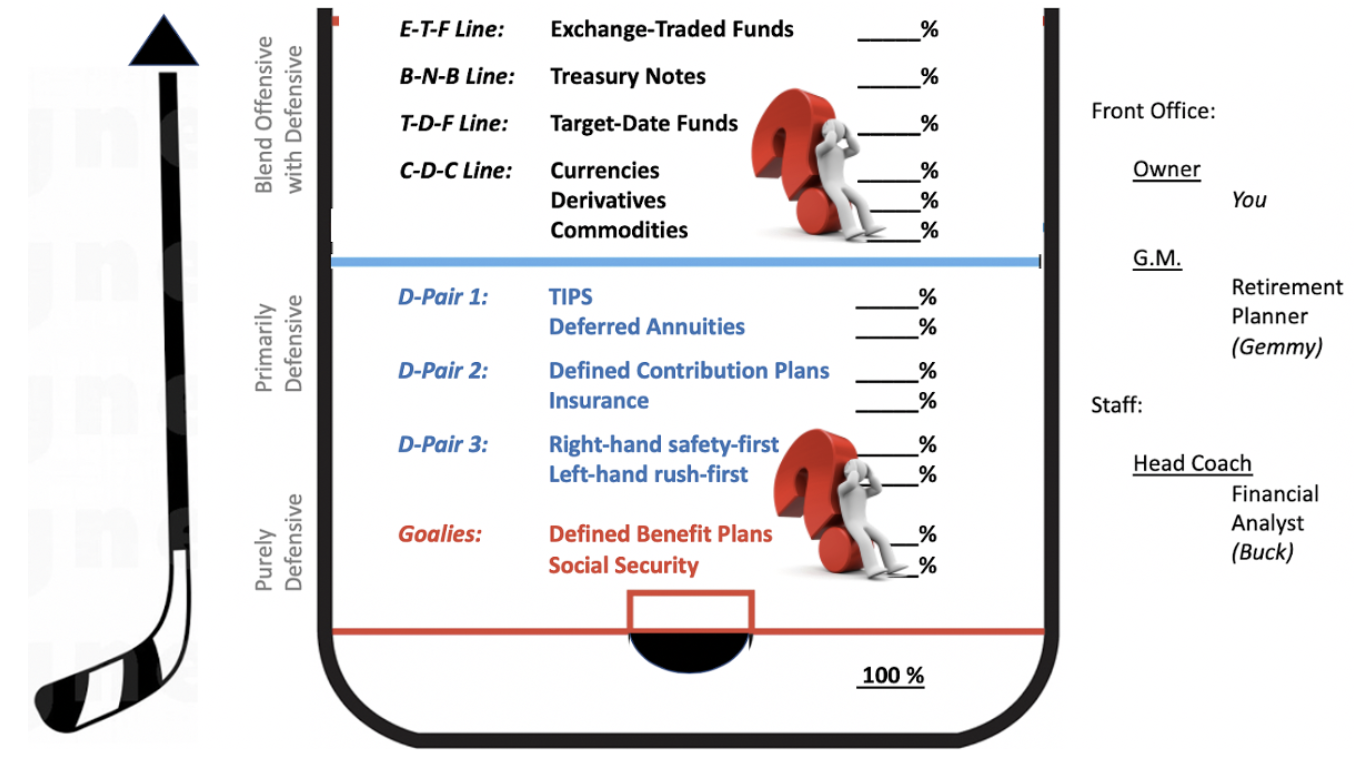

The reader can search for parallels to their own satisfaction, but a few merit comment. Note that our two goalies (Ben and Soso) are on loan from another league, so could be recalled (an involuntary “pulling the goalie”). In our parallel universe one other league is not in Europe or Russia; it is the SSA (where current forecasts are that its trust fund will be exhausted by 2035 and President Trump has indicated a preference to eliminate the payroll tax; these two sources fund 20% and 80% of Social Security payments, respectively). The other league also is local, a DBP sponsored by a corporation or state, and similarly constrained to maintain current funding. Private corporate defined benefit plans are disappearing, and public DBPs are underfunded. Even prior to the coronavirus, at least a dozen state and large municipal funds had less than half the funding needed to meet legally-obligated payouts; another dozen had less than 60%. State pension debt exceeded $1 trillion heading into 2020. The disruptions due to coronavirus clearly will exacerbate this shortfall, as state and local budgets shrink, unemployment leads to lower payroll tax contributions, and more people choose to retire early rather than find work.

Following the only completely lost season (2004-05) by an American professional sports league, the National Hockey League (NHL) imposed a financial structure on all teams. It requires every team to carry 20 (to 23) players, and for the 2019-20 season the team salary limit is $81.5M. No player can have a salary less than $700,000 or more than $16.3M. Assume the starting lineup for our team ((Ben, Tippy and Dewey, and the E-T-F Line) is paid a collective $60M, or on average $10M each. That leaves a maximum of $21.5M to divvy among the remaining 14 players, an average of about $1.5M per player. More than 2/3rds of that roster is likely to be comprised of unproven younger players or mediocre (albeit relatively well-paid) veterans. If your star center (Ted) has an expiring contract and demands $20M to resign, what to do?

Your retirement plan also has a “salary cap”; it is the total funding available to support your unknown number of retirement years. A portion of that funding is from social capital, which is payments to you and your generation based primarily on payments from the current workforce. It might be wise to view that source as “players on loan”, like our two goalies, since there is no assurance that either Social Security payments or defined benefit payments will continue, at least at current levels. There is no requirement that the remaining funding must be allocated among “the 18 skaters” on your roster, but it might be prudent to act as if NHL rules are in force.

Assume that social capital at current levels comprise 50% of your total funding for retirement. You might distribute 30% of the balance in equal payments to your six defensemen, and the remaining 20% in equal payments to your twelve forwards. If Tippy and Dewey really are a stellar defensive pairing, double your allocation to TIPS (Treasury Inflation-Protected Securities) and deferred annuities – and cut back on allocations elsewhere to compensate. You also might act as if there are imposed limits on number of players and minimum player salary. For the NHL, the current minimum salary equals only 0.86% of team cap — but it is not zero, and all twenty players get paid. A diversified retirement plan would keep all the players (goalies, d-men and forwards), make sure each contributes unique strengths, and match funding to needs.

Owning Your Retirement: Lessons from Team Owners

- Control

- Charlie Finley, MLB Oakland Athletics,1960-1980

- Jerry Jones, NFL Dallas Cowboys, 1989-

As owner of your retirement plan, how much control should you retain and how much do you delegate? Most owners of professional teams accumulated their wealth from another industry or an inheritance, and were not former players or coaches in the sport their team plays. Accordingly, they tend to take a more hands-off approach regarding day-to-day operations. However, there are exceptions, and they can be instructive for considering the level of control you may want to exert over your retirement plan. Charlie Finley was an insurance salesman, full of ideas, imagination, and himself. He championed several ideas that changed the game (like the designated hitter rule and World Series night games), and others that fell flat (like orange baseballs, adding his pet donkey Charlie O to his bullpen, and carrying the sprinter Herb Washington on his roster as a designated pinch runner: Herb appeared in 105 games as a pinch runner, but never once came to bat or otherwise took the field). Such antics alienated fellow owners, as did his abrasiveness with his own players and fans. Attention seemed his primary goal, and by that measure he was a success. As fate would have it, several future Hall of Fame players combined under his reign to bring five straight championships to Oakland, which many view as a case of random good fortune rather than ownership skill. There is a lesson here: an investor who bought a winning stock early (like Amazon) can be rich without being wise. Do not confuse good strategy with good outcomes, for elements of chance often play a major role.

Like Finley, Jerry Jones doubles as both owner and general manager of his team. Unlike Finley, or most NHL owners, Jones played the game in a highly-ranked collegiate program, where he earned all-conference selection and was co-captain of the 1964 national championship team. Soon after purchasing the Cowboys, he fired Hall of Fame coach Tom Landry and named a former teammate as replacement, then shortly thereafter named himself general manager. The team won only one game that first year. Jones did not panic, because he knew the game well and had confidence in his judgment regarding football operations and personnel. Three years later the Dallas Cowboys won the Super Bowl. To this day, Jones listens, but makes the call.

What should you directly control as the owner of your retirement plan? Three things, at least:

- Your choice of Retirement Manager and Financial Advisor

Do you qualify to be your own retirement manager and advisor? Do you want to assume one role and outsource the other? Do you outsource both roles, and if so, to one professional or two independent professionals? Going it alone can be hazardous.

- Your calibrated level of “Risk Intelligence”

Limit your direct involvement in the planning and execution to what you know, which first requires that you know what you do know and what you don’t. A Retirement Manager can help measure and calibrate your risk intelligence by asking a series of financial questions that are (i.) loosely related to funding a retirement, but (ii.) unlikely to be answered with certainty. For example, one could ask:

What is your best guess of the level of the DJIA at the beginning of 2020?

Select 2 levels such that the true level is equally likely inside or outside that interval?

If you are very confident of your best guess, then the interval should be narrow, and to the extent you are unsure of the value your interval should widen. Either way, if properly calibrated regarding what you do and don’t know, the proportion of true levels inside their associated intervals should approach 50% as the number of independent questions increases. Many people exhibit a behavioral bias known as “overconfidence”, evidenced by true values falling within the 50%-tile bands significantly less than half the time. If you exhibit this tendency toward overconfidence, then you should defer to professional advice.

- Your calibrated level of “Risk Tolerance”

How comfortable are you with the possibility of outliving your financial resources, perhaps moving into a spare room offered by your adult daughter? Are you willing to sell your home, downsize, and use any home equity proceeds to help support retirement? If your retirement plan anticipates spending 70% your current level of needs, would you make a risky investment with high upside potential that could reduce coverage to 50%? If you are enticed by the prospect of gambing for higher returns, you are “risk-prone”.

If it is very important to avoid such risks to sleep at peace, then you are “risk-averse”.

Sports team owners often are risk-prone; retirement planners tend to be risk-averse.

It often is instructive to further consider your levels of relative risk aversion:

- If you prefer to hold a smaller percentage of your assets in risky investments as your wealth increases, then you have:

- Increasing relative risk aversion

- If you prefer to hold the same percentage of your assets in risky investments as your wealth increases, then you have:

- Constant relative risk aversion

- If you prefer to hold a larger percentage of your assets in risky investments as your wealth increases, then you have:

- Decreasing relative risk aversion.

- Stability

- Peter Holt, NBA San Antonio Spurs, 1996-2016

- George Steinbrenner MLB, New York Yankees,1973-2010

The San Antonio Spurs are considered by many to be the single most successful franchise in the modern era of American competitive team sports, with the highest winning percentage and five NBA championships over the past two decades — but few fans can name their owner. He remained hands-off. By contrast, George Steinbrenner was the face of the NewYork Yankees for a generation. Championships came his way as well, but many believe that, given the market and talent advantages, many more would have but for his constant meddling — replacing the team manager 21 times in his first 23 years as owner, including hiring and firing Billy Martin five times.

Stability invariably trumps chaos, and the team (or retirement plan) owner sets that tone. Select your management and advisory team wisely, develop a plan you embrace, and stick with both.

- Flexibility

- James Dolan, NBA New York Knicks, 1999-

- Joe Lacob, NBA Golden State Warriors, 2010-

Although he had never coached before, Steve Kerr was offered two head coaching positions in 2014. Most assumed he would take the Knicks job, with the glamor and trappings of The Big Apple, and the comfort of working with Phil Jackson, the general manager who coached the Chicago Bulls to NBA championships with Michael Jordan (and Kerr) executing his patented “triangle offense”, and whom Dolan had hired after seeing that success followed by more of the same with the Lakers and Magic Johnson. But Kerr is a smart, independent thinker. He saw that the Knicks lacked an MJ or Magic, lacked stable ownership, and was looking to the past. By contrast, although the Warriors had not competed for a championship in four decades, they had fresh ownership with strong Silicon Valley roots, a data-informed approach to capitalizing on analytic insights, its pulse on the evolving future of the league, and the best shooting backcourt ever assembled, ready to exploit the 3-point trend. Kerr chose the Warriors, and so far has coached five full seasons, with five appearances in NBA Finals. A successful retirement plan owner has to remain nimble, ready to adapt to changing circumstances.

- Frugality

- Marge Schott, MLB Cincinnati Reds, 1984-1999

- Harold Ballard, NHL Toronto Maple Leafs, 1972-1990

Both these owners were notoriously cheap and universally despised, but there was a difference. Schott was a chain-smoking alcoholic and outspoken racist, who twice was suspended by the league for her discrimination against and refusal to employ people of color. She so resented high salaries of players that she made them pay for their own equipment, fly commercial, and personally handed out meal allowances herself, using dimes, nickels and pennies. Ballard also was frugal, but with purpose. He was a con man, eventually going to prison for fraud. He had little apparent interest in hockey, still less in winning games; his sole interest was making money. He was unwilling to increase payroll to improve the on-ice product, as every game was sold out regardless. As owner of your retirement plan, spend as needed for guidance to achieve goals — but no more.

… and There’s Always Next Season

Team sports share another characteristic; although the timing throughout a year varies, every sport has an annual cycle of pre-season, regular season, post-season, and off-season. The off-season is similar across sports, and regardless of win-loss record: assessments, adjustments, and actions, all in an effort to maintain or pursue outstanding performance in future seasons.

Retirement planning should be no different. Any variations in goals, significant deficiencies in performance metrics, or other relevant factors should be assessed annually with your “coaches” and “front office”, and adjustments or more substantial actions should be taken as indicated.

— Jerry Platt, Ph.D., Emeritus Professor of Finance, San Francisco State U.

Comments 365

Just simply wished to say I’m lucky I stumbled on your webpage. http://ketodietione.com/

Pingback: dating nottingham free

Acrafw – ed miracle pill Nzdxrb

Great looking site. Assume you did a great deal of your very own html coding. https://ketorecipesnew.com/

Sgbvda – medications that cause erectile dysfunction Mhvthg

thank so considerably for your website it assists a whole lot. https://ketodietplanus.com/

buy priligy 90mg – cialis singapore pharmacy canadian pharmacy viagra

https://ivermectinstr.com/# generic ivermectin

priligy dapoxetine – priligyp.com tadalafil 5mg coupon

http://ivermectinstr.online# ivermectin usa

home remedies for erectile dysfunction – ed drugs list mens ed pills

erectile dysfunction definition – ed pill latest treatment for erectile dysfunction

prednisone 5mg daily – where can i buy prednisone prednisone brand name in india

prednisone cost – deltasone costs prednisone pills

provigil generic – modafinil reddit modafinil 100 mg

prescription drugs without doctor approval: can ed be reversed – canadian online drugs

provigil for adhd – buy provigil order provigil online

accutane pill – accutane europe buy accutane online without prescription

accutane otc drug – buy accutane without prescription accutane order

canadian pharmacy online: best erection pills – online canadian pharmacy

buy amoxicillina 500 mg online – amoxicilin without prescription buying amoxicillin over the counter

amoxicillin pneumonia – generic name for amoxil amoxicillin drug

architect states not allowing hydroxychloroquine attribute https://hydroxychloroquined.online/ – hydroxychloroquine successful trials health care proxy lancet hydroxychloroquine retraction

buy vardenafil online pharmacy – vardenafil online bestellen levitra 10mg

nila vardenafil generic – vardenafil generic name buy vardenafil online no prescription

ivermectin 0.08 oral solution – ivermectin buy uk stromectola online

stromectol for humans – ivermectin 500mg ivermectin 6

cialis daily best price – tadalafil 20mg for sale cialis soft tabs original

cialis 2017 – cialis daily 2.5 mg cost online cialis pharmacy

when will viagra be generic best over the counter viagra – best place to buy viagra online

stromectol order online – stromectol generic name

buy ivermectin – stromectol

generic of accutane – accutane india accutane medication

generic viagra walmart viagra amazon – cheap viagra online

accutane cost without insurance – accutane 10mg price accutane 20 mg for sale

medication lyrica 50 mg – fstphar.com canadian pharmacy sarasota

lyrica 250 mg – reputable canadian online pharmacy canadian pharmacy world coupon code

buy amoxicillina noscript canada – amoxicillin without a doctor’s prescription price of amoxicillin 500 mg

dating sites free no registration

free online dating

tadalafil 20 mg best price in india

amoxil 500 mg – amoxicillin without dr script amoxicillin for sale

viagra 50

where to get female viagra australia – erectile dysfunction treatment where can you buy viagra without a prescription

price of viagra 100mg tablet

buy generic viagra canada – otc ed pills that work sildenafil drug coupon

doxycycline uk cost

generic viagra usa pharmacy

how to order cialis without a prescription – where to buy tadalafil 20mg tadalafil 20mg cheap

tadalafil 30mg pill – tadalafil 20mg daily cheapest tadalafil online uk

buy stromectol canada – stromectol for sale generic ivermectin for humans

best online viagra pharmacy

ivermectin cost in usa – stromectol ebay buy stromectol online

20 mg prednisone generic – fast shipping prednisone prednisone 10 mg price in india

ivermectin cost

buy prednisone tablets online – buy prednisone online without a prescription over the counter prednisone no prescription

cost of stromectol medication

ivermectin topical

stromectol pills

buy provigil online – modafinil 100mg provigil vs nuvigil

modafinil 200mg – provigil for adhd modafinil interactions

ivermectin online

azytromycyna – zithromax 250 mg zithromax otc

ivermectin 3 mg

ivermectin buy

buy stromectol canada

buy generic zithromax online – zithromax z-pak zithromax buy

ivermectin cream uk

cost of lasix – furosemide 20 mg cost cost of furosemide

ivermectin oral 0 8

stromectol online canada

ivermectin 3

lasix prescription – lasix dosage otc lasix

buy stromectol online uk

stromectol 3mg

generic stromectol

stromectol coronavirus

buy stromectol pills

buy ivermectin stromectol

tamoxifen tablets india

clomid for sale – clomid generic cheap clomid online

clomid online no prescription – clomiphene for sale clomid generic name

100 mg tadalafil

cialis price uk

sildenafil 60

online pharmacy cialis

sildenafil 5 mg tablet – sildenafil 100 mg best price generic viagra online

buy viagra online in india – viagra pills online in india viagra gel for sale uk

best pharmacy buy tadalafil

finasteride online

generic tadalafil united states

20 mg tadalafil cost – best price generic cialis 20 mg online pharmacy indonesia

generic cialis online canada – tadalafil generic daily 40 mg generic cialis

sildenafil generic india

vaigra

stromectol medication – how much does ivermectin cost stromectol coupon

cheap cialis generic online

ivermectin 3mg tablets – buy stromectol usa ivermectina 6mg

order clomid 100mg online

online casinos usa – ocean casino online casinos

buy viagra online canada

cheap viagra australia fast delivery

slot machines – gambling casino jackpot party casino

tadalafil 20mg from india

where to buy otc ed pills – over the counter erectile dysfunction pills how to cure erectile dysfunction naturally and permanently

tadalafil 5mg best price

cheap ed pills – where to buy ed pills best ed pills on the market

ivermectin 4000 mcg

ordering viagra

canadian online pharmacy prednisone – deltasone for sale prednisone 1mg purchase

800mg cialis

cialis 5mg coupon

deltasone generic – prednisonepll.com prednisone 1 mg price

Бизнесмен и меценат Максим Евгеньевич Каганский родился в Москве 19 ноября 1980 года в многодетной семье сотрудника МВД.

В 1998 году поступил в Московский Юридический Институт МВД России (сейчас

– Академия МВД России),

специальность – юрист-правовед.

максим каганский жена

максим каганский жена http://zl1.ola-cathedral.org/__media__/js/netsoltrademark.php?d=www.klerk.ru%2Fmaterials%2F2021-04-07%2Fkarelskie-rybnye-zavody-maksima-kaganskogo-popali-v-top%2F

buy doxycycline for dogs order doxycycline – doxycycline 100mg online

buy ivermectin canada

generic for plaquenil

buy generic viagra soft tabs – australia viagra prescription ordering viagra online

can you buy over the counter viagra

pinkviagraforwomen – viagra for female for sale can i buy viagra over the counter india

ivermectin coronavirus

sildenafil-citrate

generic tadalafil safe – Cialis woman order cialis in canada

stromectol price best price on ivermectin pills – stromectol tab 3mg

buy plaquenil 100mg

tadalafil price in canada – Cialis prescriptions cialis in canada cost

purchasing viagra in usa

viagra pro

cheapest tadalafil

cialis 40 mg price

ivermectin uk coronavirus – stromectol humans cost ivermectin

ivermectin stromectol – buy ivermectin for humans ivermectin 3mg price

Cheers, Quite a lot of material.

custom research paper writing services

paper writing service https://eduessaytop.com/

kamagra oral jelly price in thailand

can you buy viagra over the counter nz

mens ed pills – erectial disfunction over the counter ed pills at walgreens

otc cialis 2018

buy viagra tablet

Фильм Дом Гуччи смотреть онлайн

over the counter ed pills that work – over the counter ed treatment non prescription ed pills

order tadalafil india

cymbalta 20 mg canada

sildenafil 50mg tablets uk

modafinil 200mg online

buy sildenafil 20 mg tablets

ipratropium albuterol – ventolin price usa ventolin 90 mcg

india cialis online

order Albuterol – onventolinp.com generic ventolin

where to buy viagra over the counter

where can you buy cytotec in south africa – cytotec 200 mcg order online buy cytotec 100mcg

viagra canada online pharmacy

buy cytotec pills online cheap – cheap cytotec pills cytotec medicine price

cost of prescription viagra

cheap viagra australia fast delivery

tadalafil 60 mg for sale

buy sildenafil generic online

doxycycline 100mg capsule sale – doxycycline 20 doxycycline antimalarial

doxycycline best price – doxycycline cap 50mg doxycycline over the counter

doxycycline 100mg acne

prescription drug neurontin – neurontin 100mg tablets cost of levothyroxine brand name

sildenafil generic price

neurontin 800 mg pill – neurontin capsules 300mg levothyroxine 75 mcg tab

http://buysildenshop.com/ – Viagra

cheap brand cialis

You have made your point.

frere et soeur porno

porno siteleri https://yukon-login.ca/

viagra drug – where can you buy viagra over the counter

ivermectin 90 mg

female viagra in india online purchase – viagra 2 viagra 150 tablet

where can i buy azithromycin 500mg over the counter

смотреть фильмы

propecia sale

cost of lexapro

bio viagra

cialis 10 mg tablets – online pharmacy without prescription

cialis super active 20mg – cialis daily generic cost cialis 100mg uk

generic sildenafil online

vardenafil half life – buy brand vardenafil vardenafil cena

how to order sildenafil

sale clomid

prednisone price australia prednisone generic – can you buy prednisone in canada

vardenafil vs cialis – where to buy vardenafil in singapore buy vardenafil india

how much is trazodone cost

ivermectin 6mg dosage – buy ivermectin for humans australia

cialis for sale australia

Propecia

ivermectin 3mg dosage – india ivermectin

finasteride hair propecia for sale – finesterude no prescription

zithromax generic cost

prednisone 8 pills – prednisone price canada prednisone 6 mg

where to buy cialis without a prescription

viagra 4 tablet

prednisone without a rx – can you purchase prednisone for dogs without a prescription can you purchase prednisone for dogs without a prescription

buy real cialis online canada

buy accutane with paypal – buy generic accutane online cheap medicine accutane

accutane for sale south africa – buy cheap accutane best accutane

ivermectin brand ivermectin – ivermectin price canada

where can i buy antabuse tablets

can you buy cialis over the counter in uk

buy online cialis

http://buytadalafshop.com/ – Cialis

sildenafil canada generic

Stromectol

buy anti buse

order stromectol

http://buypropeciaon.com/ – should i take propecia

how to buy viagra cheap

accutane canada 40mg

Purchase Doryx Doxakne Usa Best Website

Генератор Дизайн человека

tadalafil 7 mg capsule

accutane over the counter

cheap cymbalta 60 mg

buy generic levitra uk

Find Amoxicilina Visa Free Doctor Consultation

ДЮНА

Соври мне правду

generic cialis from uk

9790

buy sildenafil online india

4713

8116

Kamagra Ajanta Mumbai

terramycin antibiotic ophthalmic ointment for cats

ivermectin cream 1%

doxycycline 400 mg

hydrochlorothiazide 25 mg generic

stromectol for humans

diflucan pills online

order viagra online us

order cialis from mexico

viagra prescription cost uk

low price cialis

sildenafil online in india

usa tadalafil

where can i buy viagra otc

lisinopril 20 tablet

dapoxetine 1mg

tretinoin 0025

viagra generic india

purchase viagra over the counter

cialis online safe

generic for abilify

buy abilify from india

cephalexin pharmacy

strattera 40mg cap

cialis 100mg pills

doxycycline 25mg tablets

vermox pharmacy

no rx viagra

cialis rx online

get clomid online

buspar online canada

phenergan 50 mg tablets

diflucan tablets australia

gabapentin 25mg tablets

trazodone 50 mg

cheap diflucan online

bactrim 800 mg

generic augmentin coupon

plavix medication price

levitra 5mg tablets

phenergan 25 cost

how to order amoxicillin

prescription medicine valtrex

viagra on sale

buy cephalexin online no prescription

amoxicillin over the counter in mexico

augmentin 875 mg coupon

generic levitra 80mg online

propecia buy india

amoxicillin cost

where can i buy over the counter diflucan

buy clomid cheap online

where can i buy gabapentin

citalopram prescription cost uk

where can i buy valtrex online

cost of doxycycline online canada

retino 0.05 price

can i buy bactrim online

zofran otc mexico

amoxicillin 100 mg tablets

cost of avodart

cheap tamoxifen

rx pharmacy online

xenical 120 mg buy online in india

clonidine blood pressure

zofran discount

zovirax price usa

ivermectin 24 mg

buy cheap propecia

buy nolvadex online

buy fildena 150 online

buy finasteride online 5mg

zovirax cream canada

ivermectin tablet price

albendazole drug

medicine keflex 500mg

where can i buy amoxicillin over the counter

plaquenil uk

albendozale purchase

cost of synthroid in canada

zoloft 50 mg pill

buy indocin without a prescription

robaxin 750 generic

prednisolone cost uk

prozac 2017

prednisolone uk buy

gabapentin online

tetracycline antibiotic

generic trazodone 100 mg

cheap cialis prescription

tenormin generic drug

azithromycin 200mg

where to buy strattera

erectafil 5mg

toradol iv

glucophage

buy generic amoxil no prescription

digoxin tab 125 mcg 0.125 mg

buying lexapro without a prescription

buy retin a online without a prescription

buy buspar

tretinoin prescription online

lexapro coupon

retin a prescription cost

lexapro 20mg tablet

generic for flomax

celebrex cost canada

fluoxetine 30 mg capsules

disulfiram 500 mg tablet

atarax 25 mg tablets

360 viagra

cheap generic cialis online

valtrex prices

fluoxetine 20 mg tablets

prednisolone sod

buy discount cialis

tretinoin 0.04 gel

buy amoxicillin online with paypal

buy bactrim online canada

avodart 90 capsules

xenical price comparison australia

combivent 0.5 mg 2.5 mg

ampicillin usa

buy diflucan online cheap

generic viagra paypal

buy silagra

prescription drug tizanidine

atarax buy

compare plavix prices

canadian pharmacy accutane

cialis online pharmacy us

cialis 5mg in canada

buy atarax 25mg online without rx

erectafil online

bupropion buy online india

generic for doxycycline

canadian pharmacy cialis 20mg

order clomid over the counter

gabapentin canadian pharmacy

dexamethasone 8 mg price

buy baclofen europe

valtrex generic no prescription

canada drug pharmacy

motilium 10mg

buy valtrex online canada