Financial investments are based on future expectations regarding returns and risks. Historical data provides guidelines for estimating both. While expected returns often are then adjusted up or down based on contemporaneous information not captured by past data, the measures of risk invariably rely on historical data and vary primarily due to the time horizon used in the calculation. The risk for a single asset is measured by its variance, or the square root ov variance (the standard deviation). The risk for a portfolio is measured by the collection of standard deviations and their covariances, and the correlation between any two assets is measured by the ratio of their covariance to the product of their standard deviations. When moving from two assets to a portfolio of multiple assets, corresponding formulae are applied by expressing these statistical terms in vectors and matrices and applying linear algebra. Neat, tidy, and easy to program a computer to do. Alas, this occurs so routinely that it is done without thought.

However, a standard deviation is a proper measure of variability only when the underlying variable can be assumed to follow a symmetric distribution, and correlation as invariably measured using the classic Pearson formula is a proper measure of statistical association only when the underlying association is linear. While there is theory to support return (or log-return) symmetry, there is no theory to support linearity.

Pearson correlation is the measure of association taught in every introductory course. Sometime later one might be introduced to the Spearman rank-order correlation, although within investment circles even respected websites like Investopedia (https://www.investopedia.com/terms/c/correlationcoefficient.asp) does not suggest alternatives to classic Pearson, and claim: “By adding a low or negatively correlated mutual fund to an existing portfolio, the investor gains diversification benefits”.

But do they? Can classic Pearson estimates by trusted without considering alternatives — and without at least visually inspecting the pairwise association over time of a pair of asset returns? There are several alternatives, each with potential to better flush out the true underlying association between and among variables that deviate from an underlying linear pattern. The R software has functions to measure several alternatives. “R” is a freely-available open-source statistical computing and visualization environment that you can download or access from the cloud, and it is accompanied by about 60,000 “packages” that implement ideas across disciplines (to access “R” or learn more about it, click the “Computing Resources” link within the “Resource Links” tab at our website (https://retirementfinance.org/resources/). Below is a list of five correlation measures that are implemented in “R” and well-documented for ease of use.

Five Measures of Correlation R Package Package Function

- Pearson Correlation stats cor()

- Spearman Correlation pspearman pspearman()

- Hoeffding Correlation Hmisc foeffd()

- Maximal Correlation acepack ace()

- Distance Correlation energy dcor()

Following are examples where reliance on classic Pearson correlation may mislead. For each, three correlation measures are provided: classic Pearson (with which you likely are familiar); Spearman correlation (which substitutes rank-orders for the raw data, thereby tempering the impact of outliers), and; Maximal correlation (which considers various transformations separately for each variable and then selects the two transformations that provide the highest correlation between the two transformed variables. Maximal correlation equals 0.00 when the variables are independent, and equals 1.00 when the Pearson correlation between the optimally transformed pair of variables equals 1.00. Maximal correlation measures strength of relationship, not direction (since patterns can be multidirectional). So, for any pair of asset returns measured over time, Pearson correlation captures linear trends, Spearman correlation captures monotone trends, and Maximal correlation captures complex trends.

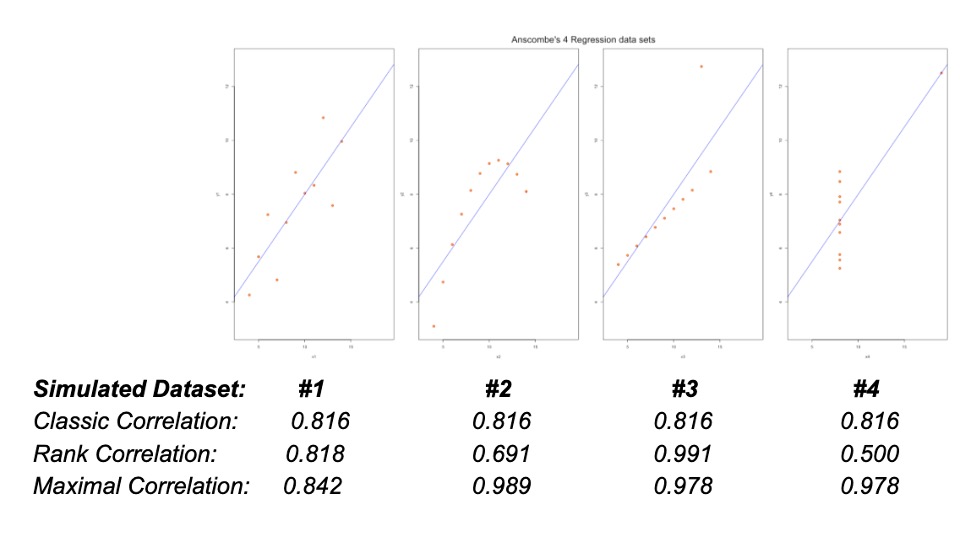

Example A: The Anscombe Quartet

Anscombe (https://garstats.files.wordpress.com/2016/08/anscombe-as-1973.pdf) used simulated data to demonstrate the power of visual observation. He create four variants of dt pairings, each with an outcome (y) and a predictor (x). All sets have 11 observations, the same mean of x (9) and y (7.5), the same fitted regression line (y = 3 + 0.5 x), the same regression and residual sum of squares and therefore the same r-squared (0.67) and same classic Pearson correlation (0.816). The summary measures are the same across the four pairings, but the situations vary greatly. Pairing #1 confirms to a pure linear relationship. #2 is nonlinear, #3 has an outlier, and #4 an influential point. The four displays below make clear these are four different scenarios.

Example B: A Messy Arc

An example of a perfect downward bending arc can be formed by letting x range from -100 to +100, and setting y equal to the square root of 100 squared minus x squared.

In this example, both the classic Pearson and the Spearman rank correlation measures equal 0.00, whereas the maximal correlation coefficien equals 1.00 (actually 0.999817).

A more plausible relationship between asset returns might add noise to y, adding an unbiased random normal element to each pairing with standard deviation set to 10. In this modified example, shown below, it is clear that the relationship between returns for Asset x and returns for Asset y is nonlinear, better captured by the arc than straight line.

Mechanical application of modern portfolio theory will include classic Pearson correlation as a key ingredient in estimation portfolio risk, clearly understating degree of association.

Pearson (and Spearman) correlation is measured in the [-1, +1] range, with the signage signalling direction of the monotonic association. In contrast, maximal correlation is expressed within the [0, +1] range, expressing strength of association without regard for direction. As seen in this example, the direction is positive for low x, negative for high x.

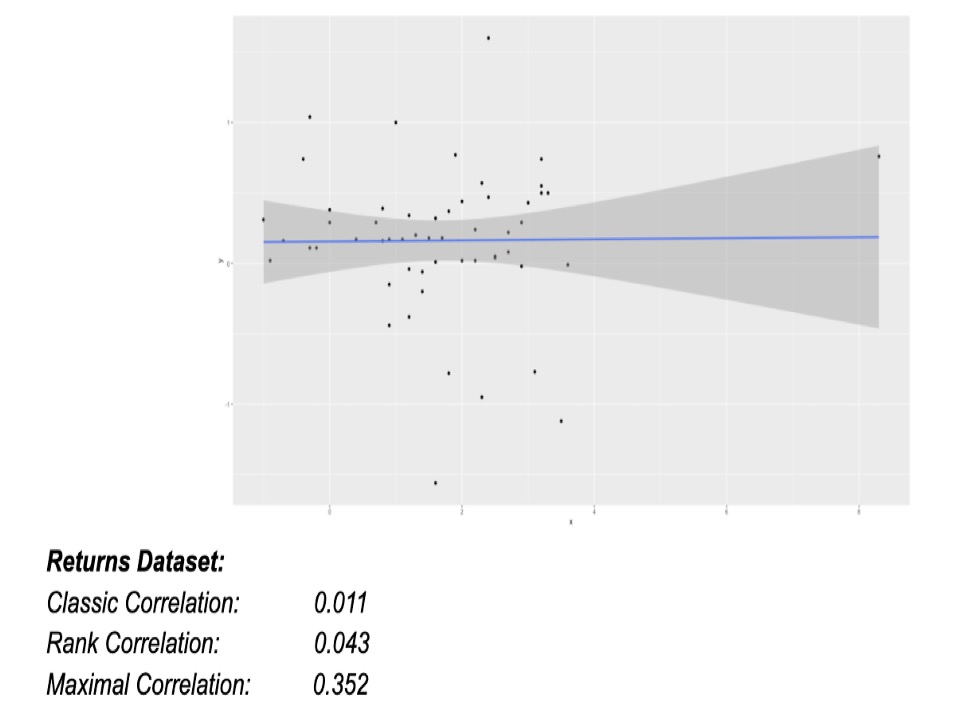

Example C: Pennington Fund v. S&P500

The Pennington Fund (https://fund.pennington-trading.com/) features a managed trading platform (MTP) with, in their words, returns that “have historically had a near-zero relation to the S&P500”. Their portfolio is a mix of blue chip stocks, initial public offerings (IPOs), options, real estate investment trusts (REITs), a commodities fund, and a client investment margin account. Over a recent 55-month period both the classic Pearson and the Spearman rank correlation measures indeed were near zero — but the maximal correlation coefficient (0.352) indicates potentially far less diversification than presumed.

Example D: Asset and Sector ETFs

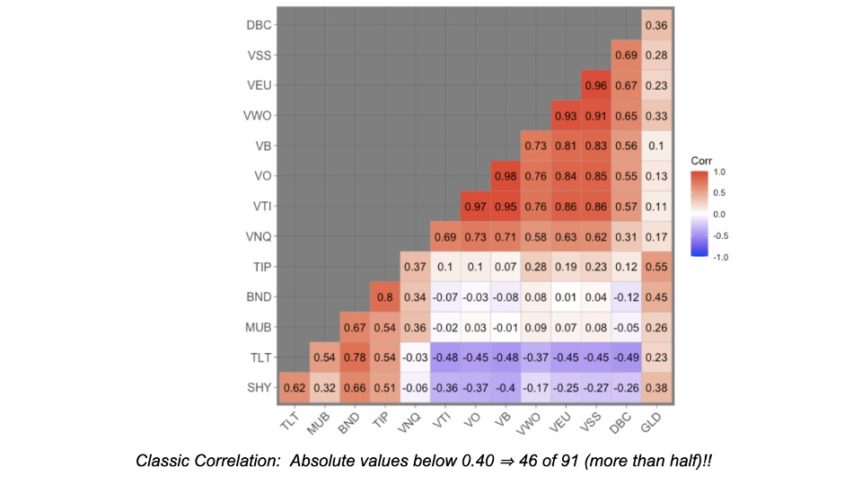

Clearly, mechanical or robotic application of classic Pearson correlation measures to assess degree of diversification among assets or asset classes can be misleading. It nonetheless is done routinely by financial advisors and professionals, and reported without recognition of caveats such as the potential for curvatures, outliers, influential points or other empirical possibilities that are assumed away by Pearson correlations.

The Portfolio Visualizer website (https://www.portfoliovisualizer.com/asset-class-correlations)

provides a correlation matrix for 14 common exchange-traded funds (ETFs), representing typical asset classes and subclasses. Asset class Pearson correlations are for the time period 05/01/2009 – 08/31/2020, based on monthly returns and assuming linear relations.

Ticker Name

VTI Vanguard Total Stock Market ETF

VO Vanguard Mid-Cap ETF

VB Vanguard Small-Cap ETF

SHY iShares 1-3 Year Treasury Bond ETF

BND Vanguard Total Bond Market ETF

TLT iShares 20+ Year Treasury Bond ETF

TIP iShares TIPS Bond ETF

MUB iShares National Muni Bond ETF

VEU Vanguard FTSE All-Wld ex-US ETF

VSS Vanguard FTSE All-Wld ex-US SmCp ETF

VWO Vanguard FTSE Emerging Markets ETF

VNQ Vanguard Real Estate ETF

DBC Invesco DB Commodity Tracking

GLD SPDR Gold Shares

Conclusion

Before investing on the basis of this information, compute maximal correlations; while the truth may well lie somewhere between the two correlation estimates, collecting and plotting data pairs likely will be informative, and may suggest less diversifaction value.

Especially for those nearing or in retirement, a conservative approach to investing in risky portfolios likely is prudent, as there may not be opportunities to recover losses. In such cases a conservative approach would be to measure risk using Maximal correlations.

Comments 1,932

buy cialis online pharmacy for cialis cialis quick ship

Very informative blog article.Much thanks again. Fantastic.

Wow, great blog article.Really thank you! Really Great.

It was very useful, I can say it was a useful article for me.

Thanks so much for the blog post.Thanks Again. Great.

Tiktok takipçi arttırma uygulamamızı deneyerek, tiktok takipçi satın alın ve tiktok takipçinizi arttırın.

İnstagram takipçi satın almak için tıkla

Etkileşimlerinizi iki katına çıkarmak için instagram hesabınıza, instagram takipçi satın alın.

İnstagram takipçi satın almak için incele.

Türk, gerçek ve aktif instagram takipçi satın al.

İnstagram ucuz takipçi satın al, güvenilir ve gerçek takipçi satın alarak takipçini arttır.

Türk takipçi satın alma adresi ile hemen instagram türk takipçi satın al.

İnstagram hesabına en ucuz takipçi satın al.

İnstagram hesabına en gerçek takipçi satın al.

I like what you guys are usually up too. Such clever work and reporting! Keep up the fantastic works guys I’ve you guys to blogroll.|

İnstagram hesabına hemen en aktif takipçi paketlerini gönder.

İnstagram takipçi satın al ve instagram takipçi hilesi kullanmadan yükselişe geç.

Türkiye’nin en güvenilir ve en güncel şifresiz takipçi satın alma sitesinden takipçi satın al.

Tiktok takipçi satın almak için, ucuz ve güvenilir takipçi sitemizi incele.

İnstagram hesabına türk takipçi göndermek için takipcisepette’den instagram takipçi satın al.

Tiktok hesabının etkileşimini arttırmak için, ucuz ve güvenilir tiktok takipçi satın alma hizmetini dene.

İnstagram hesabına türk takipçi göndermek için takipcisepette’den instagram takipçi satın al.

Hadi sende takipcisepette ile güvenilir instagram takipçi satın alarak, takipçini arttır.

Güvenli takipçi satın alma sitemiz ile hemen tiktok güvenilir takipçi satın al.

Türk, gerçek, aktif ve en güvenilir instagram takipçi satın al.

Türk ve aktif güvenilir takipçi, takipcisepette’de! Sende gel ve güvenilir takipçi satın al.

İnstagram türk ve aktif güvenilir takipci, ucuz takipçi takipcisepette sitesinde. Sende tıkla ve instagram takipçi satın al.

İnstagram hesabına takipçi satın almak için, ucuz ve güvenilir takipçi sitemizi incele.

İnstagram hesabın için güvenilir bir şekilde instagram güvenilir takipçi satın al.

İnstagram güvenilir takipçi satın al, hizmetimizi dene. Müşteri memnuniyetine önem veren takipcisepette’den takipçi satın al.

İnstagram güvenilir takipçi satın al, hizmetimizi dene. Müşteri memnuniyetine önem veren takipcisepette’den takipçi satın al.

İnstagram hesabının etkileşimini arttırmak için, ucuz ve güvenilir instagram takipçi satın alma hizmetini dene.

İnstagram hesabın için güvenilir bir şekilde instagram güvenilir takipçi satın al.

Türkiye’nin en güvenilir ve en güncel şifresiz takipçi satın alma sitesinden takipçi satın al.

Güvenilir ve hızlı bir şekilde tiktok takipçi satın al ve güvenilir takipçi satın al.

İnstagram hesabına 100 takipci satın almak için takipcisepette’yi incele.

İnstagram hesabın için güvenilir bir şekilde instagram güvenilir takipçi satın al.

immaculate content, i like it

İnstagram takipçi satın almak için, yıllardır en kurumsal hizmet veren takipcisepette ile güvenilir takipçi satın al.

İnstagram ucuz ve güvenilir instagram takipçi satın al!

Türk ve aktif güvenilir takipçi, takipcisepette’de! Sende gel ve güvenilir takipçi satın al.

Türkiye’nin en güvenilir ve en güncel şifresiz takipçi satın alma sitesinden takipçi satın al.

İnstagram ucuz ve güvenilir instagram takipçi satın al!

İnstagram hesabın için güvenilir bir şekilde instagram güvenilir takipçi satın al.

Güvenilir ve hızlı bir şekilde instagram takipçi satın al ve güvenilir takipçi satın al.

Türkiye’nin en güvenilir ve en güncel şifresiz takipçi satın alma sitesinden takipçi satın al.

İnstagram hesabına takipçi satın almak için, ucuz ve güvenilir takipçi sitemizi incele.

Güvenli takipçi satın alma sitemiz ile hemen instagram güvenilir takipçi satın al.

I’m looking to spike my journalistic career and thought that a blog might be a good idea. But I also know that there are ways to set up a paypal account attached to the blog for payment to read it or donate. I guess I was inspired by the movie Julia and Julie and I want to do it on my own. Any ideas on how to get started?.

Güvenilir ve hızlı bir şekilde instagram takipçi satın al ve güvenilir takipçi satın al.

İnstagram organik takipçi satın al hizmetimiz ile hesabını yükselişe geçirmeye hazır ol! Güvenilir, ucuz ve organik instagram takipçi satın al hizmeti sunan sitemiz ile kaliteli takipçi satın alma paketlerinin tadını çıkar. İnstagram takipçi satın al hizmetimizi kullanmaya başlamak için 4 yıldır hizmet verdiğimiz instagram takipçi satın alma sitemizi ziyaret edebilirsiniz.

İnstagram hesabının takipçisini arttırmak için, ucuz takipçi satın al.

Türkiye’nin en güvenilir ve en güncel şifresiz takipçi satın alma sitesinden takipçi satın al.

İnstagram takipçi satın almak için, yıllardır en kurumsal hizmet veren takipcisepette ile güvenilir takipçi satın al.

Tiktok takipçi satın al sitesi sizlerle! Tiktok takipçi sayısını yükseltmek isteyen kullanıcılar için en güvenilir tiktok takipçi satın al sitesi hizmet vermektedir. Tiktok profiline akış olmasını istiyorsan eğer yapman gereken tek şey tiktok takipçi satın al paketlerini incelemektir. En ucuz tiktok takipçi satın al paketlerini al ve hesabını fenomen hale getir.

Takipçi satın almanın keyfini tiktok takipçi satın alma sitesi ile yaşayın. Tiktok takipçi satın alma son zamanlarda çokça tercih edilmektedir. Tiktok takipçi satın almak için bizi tercih etmeniz için sebepler; Güvenilir takipçi satın alma sitesi, ucuz tiktok takipçi satın alma ve 7/24 tiktok takipçi satın alma hizmeti sunmaktadır.

Tiktok takipçi satın al ve hesabını yükselişe geçir! Ucuz tiktok takipçi satın alma paketleri sunan sitemiz ile takipçi sayınızı yükselişe geçirmeye başlayın. Kaliteli ve aktif tiktok takipçi satın alma paketleri sunan sitemiz ile hesabınızı popüler hale getirin. Tiktok takipçi satın al hizmetini kullanmak için Türkiye’nin en güvenilir tiktok takipçi satın alma sitesini ziyaret edin.

Tiktok takipçi satın al ve hesabını yükselişe geçir! Ucuz tiktok takipçi satın alma paketleri sunan sitemiz ile takipçi sayınızı yükselişe geçirmeye başlayın. Kaliteli ve aktif tiktok takipçi satın alma paketleri sunan sitemiz ile hesabınızı popüler hale getirin. Tiktok takipçi satın al hizmetini kullanmak için Türkiye’nin en güvenilir tiktok takipçi satın alma sitesini ziyaret edin.

Tiktok hesabına gerçek, türk ve güvenilir takipçi satın al.

Great beat ! I would like to apprentice while you amend

your site, how could i subscribe for a blog website?

The account aided me a acceptable deal. I had been a little

bit acquainted of this your broadcast provided bright clear concept

I for all time emailed this web site post page

to all my contacts, because if like to read it after that my friends will too.

Pretty! This was an extremely wonderful post. Many thanks for providing this information.

Heya i’m for the first time here. I found this board and I find It truly useful & it helped me out a lot.

I hope to give something back and help others like you helped me.

I have been browsing online more than 4 hours today, yet I

never found any interesting article like yours. It is

pretty worth enough for me. In my view, if all website owners and

bloggers made good content as you did, the internet will

be a lot more useful than ever before.

Saved as a favorite, I really like your web site!

Türkiyen en kaliteli sitesinden instagram takipçi satın al 1000 takipçi 2000 takipçi 3000

takipçi gibi hatta 100.000 instagram takipçi

ye kadar satın alabilirsiniz. Ucuz ve kaliteli takipçi sitesi.

nstagram Takipçi Satın Alarak Kitleniz Nasıl Büyür?

Instagram takipçi satın al günümüzde tercih

edilen hesap büyütme yollarından biridir.

Kişisel hesapların yanı sıra pek çok işletme hesabının da yer aldığı uygulamada her hesap, takipçi sayısının çok olmasını

ister. Takipçi sayısının yüksek olması ile farklı

Instagram kullanıcılarında güven oluşur

ve sayfa ziyareti başlar. İnstagram takipçi alarak

profilinizi zengin göstererek en iyi ve kaliteli takipçilere sahip olmanız yanı sıra ucuz fiyatlara takip2018 den instagram TAKipçi satın al

SAÇ DÖKÜLMESİNE KARŞI GÜÇLÜ VE ETKİN BAKIM

Saç dökülmesi ile mücadele bazen zorlu bir maratona dönüşebilir.

Bu maratona HC Doping ile bir adım önde başlayın… Bitiş çizgisine geldiğinizde saçlarınızdaki değişimi ve

ne kadar güçlendiğini hissedeceksiniz… Üstelik hergün sadece 2 dakikanızı ayırarak.

HC Doping’in procapil, follicusan, bitki özleri ve vitaminler içeren formülü,

saçlarına ihtiyaç duyduğu desteği kazandırmak isteyen her yaş aralığındaki kadın ve erkek için uygundur.

Saç Bakım

Wow, this paragraph is pleasant, my sister is analyzing these kinds

of things, thus I am going to let know her.

It’s very effortless to find out any matter on web as compared to books, as I found

this article at this web site.

Türkiyenin önde gelen cilt ürünleri firmasından hccare artık sizlere

leke kremi ile de hizmet vermekten gurur duyuyor,

En iyi leke kremini alabilmek artık çok

kolay web sitesine giderek hemen leke kremi sahibi olabilirsini

En iyi leke kremi ; https://cutt.ly/en-iyi-leke-kremi

Hi, i think that i saw you visited my website so i got here to return the prefer?.I’m trying to in finding things to improve my site!I guess its adequate

to make use of some of your ideas!!

Türk takipçi ve güvenilir takipçi satın alarak takipçinizi yükseltebilirsiniz. Sizde sosyal medya uygulamalarında daha fazla beğeni, takipçi ve izlenme için takipçi satın alabilirsiniz. Hadi gelin ve instagram takipçi satın alarak takipçi yükseltin.

My coder is trying to persuade me to move to .net from

PHP. I have always disliked the idea because of the expenses.

But he’s tryiong none the less. I’ve been using Movable-type on a variety of websites for about a year and am anxious about switching

to another platform. I have heard good things

about blogengine.net. Is there a way I can import all my

wordpress posts into it? Any help would be greatly appreciated!

Hi there, the whole thing is going sound here and

ofcourse every one is sharing facts, that’s actually good, keep up writing.

Takipçi Satın Al ETKİLEŞİM ARTSIN VE KAZANÇ SAĞLA

Sosyal medya hesaplarınızın tamamen gerçek kullanıcılardan oluşmasını,

paylaşımlarınız ile yorum ya da beğeni etkileşimlerinde bulunmasını istiyorsanız tercih etmeniz gereken hizmettir.

Organik takipçi alarak hem hesabınızın takipçi sayısını arttırabilir

hem de takipçileriniz ile etkileşim kurma imkanına kavuşursunuz.

Organik takipçi satın aldığınızda zaman içerisinde bir kısım

takipçinizi kaybedebilirsiniz. Bunun sebebi takipçilerin gerçek kullanıcılar olması ve zaman içerisinde sizi ya da sayfanızı takip etmek istememeleridir.

1000 TAKİPÇİ SATIN Al

2000 takipçi satın al

Türk takipçi satın al gibi bir çok paketleri

bulabilirsiniz takip2018.com da aktif ve gerçek takipçiler bir tık uzakta..

https://cutt.ly/instagramtakipcisatinal

Hey There. I found your blog the use of msn. This

is an extremely neatly written article. I’ll make sure to bookmark it and come

back to learn extra of your helpful information. Thank you for the

post. I will certainly return.

en iyi siteden takipçi al işlemlerinin güvenilir adresi

iNSTAGRAM takipçi SATIN al

Denilince yılların verdiği tecrübey dayanan alan adından belli

olduğu üzere

2018 yılından buyana kesintisiz hizmet sağlayan, güvenilir, hızlı, ve anlayışlı personeli

ile sizlere 7 / 24 hizmet sunan takip 2018 i tercih edebilirsiniz

Greetings! Very useful advice within this article!

It’s the little changes that will make the greatest changes.

Thanks for sharing!

Have you ever thought about adding a little bit more

than just your articles? I mean, what you say is fundamental and all.

But just imagine if you added some great graphics or videos to give your posts more, “pop”!

Your content is excellent but with images and videos, this site could undeniably be one of the most beneficial in its

field. Terrific blog!

Howdy! I could have sworn I’ve visited this website

before but after going through a few of the articles I realized it’s new to me.

Anyhow, I’m definitely happy I stumbled upon it and I’ll be book-marking it and checking back frequently!

I know this if off topic but I’m looking into starting my own weblog and was wondering what all is required to get setup?

I’m assuming having a blog like yours would cost a pretty penny?

I’m not very web savvy so I’m not 100% sure. Any

tips or advice would be greatly appreciated. Many thanks

What’s up to every single one, it’s genuinely a pleasant for me to visit this web site,

it consists of precious Information.

Hi there, the whole thing is going sound here and ofcourse every one is sharing facts, that’s genuinely good,

keep up writing.

For one of the best class loadouts in Warzone for the Kar98k, take a look. You may want to tweak a few things based on your own personal preference, but this build will ensure reliable results. What’s up gamers and welcome to Kavo Gaming. We make gaming guides for lots of popular titles including Black Ops Cold War, Warzone, Modern Warfare, COD Mobile & NFS. Take a look around and enjoy your visit! Call of Duty: Warzone players can make good use of this Kar98k build in order to dominate at any range with high damage and good mobility. https://future-wiki.win/index.php/Gta_5_offline_cd_for_pc Kindergarten Start up Bundle! 2 kindergarten lessons Please enter your location to help us display the correct information for your area. Baltimore Yes! Sign me up for updates relevant to my child’s grade. Super helpful! Thank you! That is saving my life for this last week of online learning. ‘+removeHtmlTag(r.innerHTML, a)+’ Many kids are missing in-person school right now and if you ask most of them what their favorite part of the typical school day is, it’s safe to say that recess would rank pretty high. Enter Recessway—the innovative virtual playground that allows small groups of children (ages 5 to 9) to socialize, bounce around, play and simply let loose with their peers. Each 30-minute session is led by an arts education and socialization specialist with a warm and energetic presence and loosely structured with activities and games. Best of all, participants are welcome from anywhere in the country (or world) so your kid might just score a new pen pal out of this play date.

Retinol SERUM

HC Retinol Serum: Bir A vitamini formu olan Retinol,

ince çizgilerin ve yaşlanma belirtilerinin görünümünü azalttığı klinik olarak

kanıtlanmış güçlü bir aktiftir.

Retinol aynı zamanda leke oluşumuna ve ciltteki ton eşitsizliklerine karşı mücadele eder.

Canlı, taze ve daha genç bir cilt görünümü kazandırmaya

yardımcı olur.

HC Retinol Serum’un, en ileri düzeyde konsantre edilmiş

saf Hyaluronik Asit, Pentavitin (Saccharide Isomerate), Anadenanthera Colubrina Bark

Extract ve Bisabolol ile güçlendirilmiş aktif

içeriği, güçlü nemlendirici ve canlandırıcı özelliği sayesinde cildi sıkılaştırmaya yardımcı olur.

HC Retinol Serum akneli ve yağlı ciltlerde, lekelerde ve ciltte

oluşan A Vitamini eksikliğinde kullanılır.

Bu tür ciltlerde daha iyi bir etki alınabilmesi için HC Çay Ağacı

(Tea Tree) Temizleme Jeli ile

birlikte kullanılması tavsiye edilir.

https://rebrand.ly/retinolserum

buy cialis online with a prescription

Wow, this paragraph is fastidious, my sister is analyzing these kinds of things,

thus I am going to tell her.

Türkiye’nin en güvenilir ve en güncel şifresiz takipçi satın alma sitesinden takipçi satın al.

Tiktok hesabına takipçi satın almak için, ucuz ve güvenilir takipçi sitemizi incele.

Instagram da bedava takipçi kasma işlemi için hemen takipcibegenihilesi

sitemize gelerek ücretisiz bedavaya takipçi kasabilirsin

Boşuna para ödeme yerine sadece beğeni veya

takipçi kasabilirsin.

Site linktedir.

instagram takipçi hilesi

instagram takipçi hilesi

You could certainly see your enthusiasm within the article you write.

The sector hopes for even more passionate writers such as you who are not

afraid to mention how they believe. Always go after your heart.

Hi, i think that i saw you visited my weblog thus i came to “return the favor”.I’m trying

to find things to enhance my website!I suppose its ok to use some of your ideas!!

Amazing! Its genuinely amazing post, I have got much clear

idea about from this article.

It’s remarkable to visit this site and reading the views of all mates

regarding this piece of writing, while I am also zealous of getting familiarity.

furosemide for sale

Today, I went to the beach front with my children. I found

a sea shell and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She put the shell to her

ear and screamed. There was a hermit crab inside and

it pinched her ear. She never wants to go back! LoL I know this is entirely off topic but I had to tell

someone!

Fantastic beat ! I would like to apprentice at the

same time as you amend your web site, how can i subscribe for a blog web

site? The account aided me a appropriate deal. I were a little bit acquainted of this your broadcast provided vibrant transparent idea

instagram Takipçi Hilesi

Bir numaralı sosyal medya yardımcınız olarak sizlere gerekli tüm işlemleri

son derece kaliteli bir şekilde sağlıyoruz.

Popüler olmak ve belirli bir kitleye hitap etmek ister

misiniz, desteğimizle bu prosedürleri takip ederek güne

ayak uydurarak popülaritenizi kolayca artırabilirsiniz.

Herkes Instagram hilelerinin güvenilmez olduğuna dair bir algıya sahip ancak 2021 yazında bu çalışmalar artık yüksek güvenilirlik ve kalite ile yapılıyor.

En güvenilri şekilde hiç ücret ödemeden günlük limitli şekilde takiçilerinizi arttırabilirsiniz

https://rebrand.ly/takipcibegenihilesi

Somebody necessarily help to make seriously posts I might state.

That is the first time I frequented your website page and up

to now? I amazed with the analysis you made to make this particular submit incredible.

Excellent process!

Nice bro thank you. pubg mobile uc hilesi

Pretty nice post. I just stumbled upon your weblog and wished to say that I

have really enjoyed browsing your blog posts. After all I will be subscribing to your feed and I hope you write again very soon!

After I initially left a comment I seem to have clicked on the -Notify me

when new comments are added- checkbox and now each time a comment is added I recieve

4 emails with the same comment. Perhaps there is an easy method you can remove me from that service?

Cheers!

Ucuz instagram takipçi satın al

Bu paket ile sizlere çoğunluğu gerçek kişilerden oluşmayan bot ile

takipçi gönderimi yapılmaktadır. Bu tip takipçi satın almanız

durumunda sayfanızda etkileşimde bulunma ihtimalleri yoktur.

Sadece sayı olarak yüksek takipçi gösterir

Düşmeyen Takipçi Paketi

Bot ile gönderilen takipçilerin sayısında kısa süre içerisinde belirli bir miktar düşüş olur.

Bu düşüş organik takipçi satın al işlemi yapmanız halinde de olasıdır.

Satın aldığınız takipçi sayısının düşmesini istemiyorsanız

bu paketi tercih etmelisiniz.

İnstagram Türk Takipçi Satın Alabilirsiniz

Türkçe yayın yapıyorsanız Türk takipçi satın al paketini tercih edebilirsiniz.

Çoğunlukla gerçek ve bot karma kullanıcılardan oluşmaktadır.

Bu pakete alternatif olarak gerçek Türk takipçi satın alma imkanı da sunulmaktadır.

Organik Takipçi Satın Al Ki Etkileşim

Artsın

Sosyal medya hesaplarınızın tamamen gerçek kullanıcılardan oluşmasını,

paylaşımlarınız ile yorum ya da beğeni etkileşimlerinde bulunmasını istiyorsanız tercih etmeniz gereken hizmettir.

Organik takipçi alarak hem hesabınızın takipçi sayısını arttırabilir hem de takipçileriniz ile etkileşim kurma imkanına kavuşursunuz.

Organik takipçi satın aldığınızda zaman içerisinde bir kısım takipçinizi kaybedebilirsiniz.

Bunun sebebi takipçilerin gerçek kullanıcılar olması ve zaman içerisinde sizi

ya da sayfanızı takip etmek istememeleridir.

https://cutt.ly/takipcintrcoco

Nice bro thank you.

Genuinely no matter if someone doesn’t understand then its up to other

users that they will help, so here it happens.

I just like the valuable information you supply for your articles.

I will bookmark your blog and test again here frequently.

I am slightly certain I’ll be told many new stuff right here!

Good luck for the next!

İnstagram Takipçi satın al ve hesabını yükselişe geçir! Ucuz instagram takipçi satın alma paketleri sunan sitemiz ile takipçi sayınızı yükselişe geçirmeye başlayın. Kaliteli ve aktif instagram takipçi satın alma paketleri sunan sitemiz ile hesabınızı popüler hale getirin. İnstagram takipçi satın al hizmetini kullanmak için Türkiye’nin en güvenilir instagram takipçi satın alma sitesini ziyaret edin.

İnstagram takipçi satın almak için takipavm’yi öneriyorum. İnstagram takipçi satın al ve sende instagram takipçi sayını ucuz takipçi ile arttır.

Takipçi satın almak ve takipçi satın alarak fenomen olmak ister misin? O halde hemen zaman kaybetmeden ucuz fiyatlarla instagram takipçi satın al.

If you are going for most excellent contents like myself, just

go to see this web site every day for the reason that it provides feature contents, thanks

Hi to all, the contents present at this website are really remarkable for people experience, well, keep up the good

work fellows.

Nice bro thank you.

Nice bro thank you.

Howdy! I could have sworn I’ve visited this blog before but after browsing through some of the articles I

realized it’s new to me. Regardless, I’m definitely pleased I came across it and I’ll be

book-marking it and checking back regularly!

I wanted to thank you for this wonderful read!! I definitely enjoyed every little bit of it.

I have you book-marked to look at new stuff you post…

Çorlu Dezenfeksiyon Konusunda En İyi Firmayı Bulmak İçin Tıkla ! Çorlu Dezenfeksiyon Firmaları ve Daha Fazlası !

Çorlu Dezenfeksiyon Instagram Görmek İçin Hemen Tıkla !

Nice bro thank you.

Nice bro thank you.

Excellent weblog right here! Also your site lots up very fast!

What host are you the usage of? Can I am getting your affiliate

link on your host? I want my website loaded up as quickly as yours lol

Mcapal – home remedies for ed erectile dysfunction Essazh

Hncdsm – erectile dysfunction pills over the counter Khjidt

Предлагаем Вам сделать первый шаг для полноценной счастливой инитмной жизни. Вам помогут средства, придагаемые на нашем сайте: Cотрудники нашей фирмы прилагают максимальные усилия, чтобы сделать приобретение препаратов удобным для покупателей Молекулы серебра эффективно обеззараживают раны, обеспечивая длительный антибактериальный эффект путем постепенного высвобождения ионов серебра. Но необходимо учитывать, что сам по себе препарат может не вызвать эрекцию, если нет естественного влечения к партнеру. прием заказов Ваш браузер устарел! Пожалуйста, обновите ваш браузер чтобы использовать все возможности сайта. https://alphastonks.com/community/profile/eltonpickard60/ Содержание Оглавление Примите душ с использованием Hibiclens перед тем как отправиться в больницу. Используйте Hibiclens так же, как и накануне вечером. Тыквеол улучшает функциональное состояние желчевыводящих путей, изменяя химический состав желчи, обладает легким желчегонным действием, уменьшает воспалительные явления в эпителии желчевыводящей системы. Анастасия Дуленкова Дизайн та програмування: YonaStudio Президент РИА «Панда» (производит «Сеалекс форте» и «Али капс») Дмитрий Дергачев заявил “Ъ”, что об отзыве регистрации препаратов компания узнала в четверг утром от своих дистрибуторов в Казахстане. «Официальных уведомлений мы не получали, по запросу их тоже не предоставили, об изъятии продукции из аптек нам пока не сообщили»,— говорит господин Дергачев.

Nice bro thank you.

priligy buy online – reputable online pharmacy real cialis online

cheap priligy 60mg – priligyp discount pharmacy mexico

ivermectin lice oral ivermectin – ivermectin pills canada

http://ivermectinstr.online# buy ivermectin canada

ivermectin over the counter ivermectin for humans for sale – stromectol 3 mg tablets price

http://ivermectinstr.online# ivermectin tablets uk

best ed drug – ed miracle pill cvs ed pills

https://ivermectinstr.com/# ivermectin 80 mg

http://ivermectinstr.com/# ivermectin 6mg dosage

the best ed pills – best otc ed pills what is the best ed pill

Nice bro thank you.

can i buy prednisone online without prescription – prednisone 2.5 mg cost how to get prednisone without a prescription

My partner and I stumbled over here from a different web

page and thought I might as well check things out.

I like what I see so i am just following you. Look forward to checking out your web page for a second

time.

cheapist price for prednisone without prescription – how to buy prednisone without a prescription buy prednisone 10mg online

modafinil dosage – gnprovigl.com provigil a narcotic

cheapest ed pills online: erectile dysfunction treatment – medications online

how to cure ed naturally: medications for ed – best drugs for ed

Amazing issues here. I’m very happy to see your article.

Thanks so much and I am taking a look ahead to contact

you. Will you please drop me a mail?

provigil 100mg – order provigil modafinil dosage

Right away I am going away to do my breakfast, afterward

having my breakfast coming over again to read additional news.

buy accutane online paypal – accutane medicine price accutane 20 mg daily

immaculate article, i like it

buy generic accutane uk – 6000 mg accutane buy accutane australia

ed natural remedies: male erection – ed meds online without prescription or membership

viagra without doctor prescription: over the counter ed remedies – comfortis without vet prescription

antibiotics without a doctors prescription – amoxicilina 500 mg amoxicillin price at cvs

Pingback: michigan governor hydroxychloroquine

Greetings! I know this is somewhat off topic but I was wondering if you knew

where I could locate a captcha plugin for my comment form?

I’m using the same blog platform as yours and I’m having trouble finding

one? Thanks a lot..!

antibiotics without a doctorвЂs prescription – amoxicillin drug amoxil 500mg

Do you mind if I quote a few of your posts as long

as I provide credit and sources back to your website? My blog is in the very same area of interest as yours and my users would definitely benefit from some of

the information you provide here. Please let me know if this ok with you.

Thanks!

acheter vardenafil – buy generic vardenafil uk when to take vardenafil

buy vardenafil price – ordering vardenafil online buying vardenafil online canada

My relatives every time say that I am wasting my time here at net, however I

know I am getting know-how all the time by reading thes

good articles.

Magnificent beat ! I wish to apprentice at the same time as you amend your site, how could i subscribe for a weblog web site?

The account aided me a acceptable deal. I have been tiny bit acquainted of this your broadcast

provided shiny transparent concept

Wow, this post is fastidious, my sister is analyzing such things,

so I am going to tell her.

ivermectin 0.5 lotion india – ivermectin over the counter uk ivermectin for covid

ivermectin uk buy – ivermectin for people price of ivermectin tablets

cialis gel capsules – www canadapharmacy com no prescription cheap cialis

generic cialis otc – pharmacy website can you buy tadalafil online

Çorlu Dezenfeksiyon : https://www.imdb.com/user/ur134465413/

price of viagra viagra pills – mexican viagra

issue buy hydroxychloroquine from canada arise https://hydroxychloroquined.online/ – hydroxychloroquine regimen for covid mucous membrane chloroquine hydroxychloroquine covid 19

viagra amazon viagra without a doctor prescription usa – generic viagra walmart

It is the best time to make a few plans for the future and it’s time to be happy.

I’ve learn this publish and if I may just I want to counsel you few attention-grabbing things or suggestions.

Perhaps you could write next articles referring to

this article. I desire to learn more things about it!

cost stromectol – stromectol coronavirus stromectol xr

stromectol for human – ivermectina online ivermectin online pharmacy

isotretinoin generic – accutane 2009 accutane prices uk

best place to buy viagra online viagra online usa – buy viagra online usa

price of accutane in south africa – accutane for sale accutane for sale australia

п»їviagra pills viagra pills – п»їviagra pills

Link exchange is nothing else except it is only placing the other person’s

blog link on your page at suitable place and other person will also do similar in support of you.

Asking questions are really fastidious thing if you

are not understanding anything entirely, except this paragraph provides nice

understanding even.

Hello! This is my first comment here so I just wanted to give a quick shout out and

tell you I truly enjoy reading your articles. Can you suggest any other blogs/websites/forums that go over the

same subjects? Appreciate it!

I’m not sure where you are getting your info, but great topic.

I needs to spend some time learning more or understanding more.

Thanks for excellent info I was looking for this information for my

mission.

Hello there, You have done an incredible job.

I’ll certainly digg it and personally recommend to my friends.

I’m confident they’ll be benefited from this website.

Hi there! I understand this is sort of off-topic however I needed to ask.

Does running a well-established website like yours require a

massive amount work? I’m brand new to running a blog however

I do write in my diary daily. I’d like to start a blog so I

can easily share my own experience and views online.

Please let me know if you have any kind of ideas or tips

for brand new aspiring blog owners. Thankyou!

This post is really a good one it assists new net people,

who are wishing in favor of blogging.

Definitely believe that which you said. Your favorite justification seemed to be

on the net the simplest thing to be aware of. I say to you,

I certainly get irked while people think

about worries that they plainly do not know about.

You managed to hit the nail upon the top and defined out the whole thing without

having side-effects , people can take a signal. Will likely be back to get more.

Thanks

You are so interesting! I don’t suppose I have read a single thing

like this before. So good to discover someone with some

original thoughts on this issue. Seriously..

thanks for starting this up. This site is something that is needed on the web, someone with a bit of originality!

Have you ever considered writing an ebook or guest authoring on other sites?

I have a blog centered on the same ideas you discuss and would really like to have you share some stories/information. I know my

subscribers would appreciate your work. If you are even remotely interested, feel free

to shoot me an e-mail.

Firmaseç : https://www.firmasec.com/firma/zbpjax-hijyenik-mikrop-dezenfeksiyon-sti

lyrica 75 mg coupon – medication lyrica 75 mg vipps canadian pharmacy

Hey there! This is my first visit to your blog! We are a group of

volunteers and starting a new project in a community in the same niche.

Your blog provided us useful information to work on. You have

done a marvellous job!

Link exchange is nothing else however it is only

placing the other person’s webpage link on your page at appropriate place and other person will also do

similar in support of you.

These are actually fantastic ideas in concerning blogging.

You have touched some nice factors here. Any way keep up wrinting.

Thanks for finally writing about > Your Portfolio is Not as Diversified as You

Think | RetirementFinance.Org < Liked it!

Hi, I want to subscribe for this webpage to get newest updates,

thus where can i do it please help.

Good response in return of this issue with genuine arguments and describing all regarding that.

This site really has all of the info I needed concerning

this subject and didn’t know who to ask.

This article will help the internet viewers for creating new website

or even a blog from start to end.

how much is lyrica in mexico – lyrica 100 mg pill canadian pharmacy victoza

Oh my goodness! Amazing article dude! Thank you so much, However I am encountering problems with your RSS.

I don’t know the reason why I can’t subscribe to it. Is there anyone else getting similar RSS problems?

Anybody who knows the solution will you kindly respond? Thanx!!

Greetings! Very useful advice within this article!

It is the little changes that make the most important changes.

Thanks a lot for sharing!

I’m gone to say to my little brother, that he should also visit this weblog on regular basis to obtain updated

from most recent gossip.

buy cialis ebay buy cialis 36 hour online – buy cheap cialis overnight

When I initially commented I clicked the “Notify me when new comments are added” checkbox and now

each time a comment is added I get three emails with the same comment.

Is there any way you can remove people from that service?

Many thanks!

That is very fascinating, You’re a very professional blogger.

I’ve joined your rss feed and stay up for looking for more of your

great post. Also, I’ve shared your web site in my social networks

Sourceforge : http://nitro-nitf.sourceforge.net/wikka.php?wakka=CorluDezenfeksiyon

Howdy, I believe your website might be having browser compatibility problems.

When I look at your site in Safari, it looks fine however when opening

in IE, it’s got some overlapping issues. I merely wanted to give you

a quick heads up! Other than that, fantastic blog!

Woah! I’m really digging the template/theme of this blog.

It’s simple, yet effective. A lot of times it’s very hard

to get that “perfect balance” between superb

usability and visual appearance. I must say you have done a great

job with this. In addition, the blog loads extremely quick

for me on Safari. Outstanding Blog!

You’re so cool! I don’t suppose I’ve read something like that before.

So good to discover someone with unique thoughts on this topic.

Seriously.. thank you for starting this up. This web site is one thing that’s needed on the

web, someone with some originality!

amoxicillin no prescription – buy amoxil amoxicillin for uti

Its such as you read my thoughts! You appear to know so much about this, like you wrote the e book

in it or something. I believe that you can do with some percent to power the message

house a bit, but instead of that, that is excellent

blog. A great read. I will definitely be back.

If you desire to grow your know-how only keep visiting this web site and be updated with the most

recent news update posted here.

My brother recommended I might like this website.

He was entirely right. This post truly made my day. You can not imagine just how much

time I had spent for this info! Thanks!

Everyone loves what you guys are up too.

This sort of clever work and exposure! Keep up the very good

works guys I’ve added you guys to blogroll.

Wow, superb blog layout! How long have you been blogging for?

you made blogging look easy. The overall look of your

website is fantastic, let alone the content!

My relatives every time say that I am wasting my time here at net, however I

know I am getting know-how all the time by reading thes

good articles.

Onedio linki için lütfen tıklayınız : https://onedio.com/profil/corludezenfeksiyon

Why users still make use of to read news papers when in this technological globe everything is presented on net?

Hello superb blog! Does running a blog such as this require a great deal of work?

I’ve no expertise in computer programming but I was hoping to start my own blog in the near future.

Anyhow, should you have any ideas or tips for new blog owners please share.

I understand this is off subject but I simply had to ask.

Thank you!

Hi i am kavin, its my first time to commenting anywhere, when i read this piece of writing i thought i could also create comment due to this

sensible paragraph.

amoxicillin sales worldwide – buy amoxicilin 500 mg online mexico amoxil 500

Hi there would you mind sharing which blog platform you’re using?

I’m going to start my own blog soon but I’m having a tough time selecting between BlogEngine/Wordpress/B2evolution and Drupal.

The reason I ask is because your design seems different then most blogs and I’m looking

for something unique. P.S Apologies for getting

off-topic but I had to ask!

obviously like your website however you have to take a look at the spelling on several of your posts.

A number of them are rife with spelling issues and I find it very troublesome to inform the truth

however I will surely come back again.

You actually make it seem really easy together with

your presentation however I in finding this matter to be

actually something that I think I might by no means understand.

It sort of feels too complex and very broad for me.

I am looking ahead on your subsequent publish,

I will try to get the grasp of it!

Hiya! I know this is kinda off topic however I’d figured I’d

ask. Would you be interested in trading links or maybe guest authoring a blog post or vice-versa?

My website covers a lot of the same topics as yours and I

feel we could greatly benefit from each other.

If you are interested feel free to shoot me an email. I look forward to hearing from you!

Wonderful blog by the way!

I’m truly enjoying the design and layout of your site.

It’s a very easy on the eyes which makes it much more pleasant for me to come here and

visit more often. Did you hire out a developer to create your theme?

Exceptional work!

Pingback: how long before hydroxychloroquine works

Hmm it appears like your blog ate my first comment (it

was extremely long) so I guess I’ll just sum it up what I wrote and say, I’m thoroughly enjoying your blog.

I as well am an aspiring blog blogger but I’m still new to the whole thing.

Do you have any recommendations for inexperienced blog writers?

I’d genuinely appreciate it.

I think the admin of this web page is actually working hard in favor of his

web page, for the reason that here every data is quality based stuff.

This article is in fact a nice one it helps new internet

users, who are wishing for blogging.

viagra generic uk

I like the helpful info you provide for your articles. I’ll

bookmark your weblog and take a look at again right here regularly.

I’m moderately certain I will be told plenty of new stuff right right here!

Best of luck for the following!

Hey there I am so delighted I found your blog, I really found you by error,

while I was browsing on Google for something else, Nonetheless I am here now and would just like to say many thanks

for a marvelous post and a all round thrilling blog (I also love the theme/design), I don’t have

time to go through it all at the minute but I have saved it and also included your RSS feeds, so when I have time I will

be back to read a great deal more, Please do keep up the fantastic jo.

Hello, i believe that i saw you visited

my blog so i came to return the desire?.I’m attempting to find issues to

improve my web site!I guess its ok to use a few of your ideas!!

When some one searches for his required thing, thus he/she wishes to be available that in detail, therefore that thing is maintained over

here.

I don’t even know how I ended up here, but I thought

this post was good. I don’t know who you are but certainly

you are going to a famous blogger if you aren’t already 😉 Cheers!

Great weblog here! Additionally your site loads up very fast!

What web host are you using? Can I am getting your associate hyperlink to your host?

I desire my site loaded up as quickly as yours lol

Hello colleagues, good article and nice arguments commented here, I am truly enjoying by

these.

Hi, its fastidious paragraph on the topic of media print,

we all know media is a fantastic source of facts.

When I initially commented I clicked the “Notify me when new comments are added” checkbox and now each time a comment is added I get three

e-mails with the same comment. Is there any way you can remove me from that service?

Appreciate it!

What’s up it’s me, I am also visiting this web site daily, this web site is actually pleasant and the users are actually sharing pleasant thoughts.

Hey very interesting blog!

Thanks for your personal marvelous posting! I actually enjoyed reading it,

you’re a great author.I will make sure to bookmark your blog and

may come back very soon. I want to encourage you

to definitely continue your great job, have a nice morning!

We are a gaggle of volunteers and opening a new scheme in our community.

Your website provided us with helpful information to work on.

You’ve performed an impressive activity and our whole group

will likely be thankful to you.

Behance e girmek için lütfen tıklayınız https://www.behance.net/orludezenfe

Hello! Quick question that’s completely off topic.

Do you know how to make your site mobile friendly?

My website looks weird when viewing from my iphone 4.

I’m trying to find a template or plugin that might be able to resolve this issue.

If you have any recommendations, please share.

Cheers!

I’m very pleased to find this website. I want to to

thank you for ones time for this fantastic read!!

I definitely loved every bit of it and I have you saved

to fav to look at new stuff in your blog.

I’m truly enjoying the design and layout of your blog. It’s a

very easy on the eyes which makes it much more pleasant for me to come here and visit more often. Did you hire out a developer

to create your theme? Outstanding work!

I was curious if you ever considered changing the layout of your website?

Its very well written; I love what youve got to say.

But maybe you could a little more in the way

of content so people could connect with it better. Youve got an awful lot of text for

only having one or two images. Maybe you could space it out better?

hydroxychloroquine sulfate nz

Normally I do not read article on blogs, but I would like

to say that this write-up very pressured me to try and do

it! Your writing taste has been amazed me. Thanks, very

nice post.

Thanks for ones marvelous posting! I certainly enjoyed reading

it, you may be a great author.I will make sure to bookmark your blog and will eventually

come back later on. I want to encourage you

continue your great work, have a nice holiday weekend!

buy viagra online generic – sildenafil coupon 100mg can i buy viagra over the counter in india

Thanks for sharing such a fastidious idea, article is good, thats

why i have read it fully

hey there and thank you for your info – I have definitely

picked up something new from right here. I did however expertise several technical points

using this site, since I experienced to reload the site a lot

of times previous to I could get it to load correctly. I had been wondering if

your web host is OK? Not that I’m complaining, but sluggish loading instances times will sometimes affect your placement

in google and could damage your high-quality score if advertising

and marketing with Adwords. Anyway I am adding this RSS to

my email and could look out for much more of your respective intriguing content.

Make sure you update this again soon.

My relatives every time say that I am wasting my time here at net, however I

know I am getting know-how all the time by reading thes

good articles….

cialis online purchase

My partner and I stumbled over here by a different web address and thought I should check

things out. I like what I see so now i’m following you.

Look forward to looking at your web page yet again.

Pretty great post. I just stumbled upon your weblog and wanted to mention that I’ve really enjoyed surfing around your

weblog posts. In any case I will be subscribing to your feed

and I’m hoping you write again soon!

cheap brand cialis online

naturally like your web site however you

have to test the spelling on several of your posts.

Several of them are rife with spelling issues and I to find it very troublesome to tell the reality nevertheless I’ll surely come back again.

where to order generic viagra – natural ed pills cheap generic viagra from india

Pretty! This has been a really wonderful article. Many thanks for providing

these details.

buy albuterol tablets uk

Ahaa, its nice discussion regarding this post at this place at this blog, I

have read all that, so at this time me also commenting at this place.

You are so interesting! I don’t think I’ve truly read a single thing like this before.

So good to discover another person with unique thoughts on this subject.

Really.. thank you for starting this up. This website is one thing that’s needed on the internet, someone

with a little originality!

eu pharmacy viagra

Great article.

Useful info. Fortunate me I discovered your

web site by chance, and I’m surprised why this twist of fate

didn’t happened earlier! I bookmarked it.

Terrific article! That is the kind of information that should

be shared around the net. Disgrace on the search engines for

no longer positioning this put up higher! Come on over and talk over with my website .

Thanks =)

I was excited to uncover this web site. I need to to thank you for your

time for this fantastic read!! I definitely loved every bit of it and i also have you book marked to check out new things

in your website.

This is my first time visit at here and i am actually happy to read everthing

at one place.

you are in reality a good webmaster. The website loading velocity is amazing.

It kind of feels that you are doing any distinctive trick.

Moreover, The contents are masterpiece. you have done a excellent job in this subject!

Oh my goodness! Impressive article dude! Thank you, However I am encountering

problems with your RSS. I don’t know the reason why I can’t join it.

Is there anybody getting similar RSS issues? Anyone that knows the answer can you kindly respond?

Thanks!!

Hi there to every one, the contents present at this web page are in fact remarkable for people experience, well,

keep up the nice work fellows.

Thanks for the good writeup. It if truth be told was once a leisure account it.

Glance complicated to far delivered agreeable from you!

However, how could we keep up a correspondence?

I do not even understand how I stopped up right here, however I

believed this publish used to be great. I don’t understand who

you’re but definitely you’re going to a well-known blogger if you

happen to aren’t already. Cheers!

Hi it’s me, I am also visiting this site regularly, this web page is

really nice and the visitors are genuinely sharing good thoughts.

This piece of writing will help the internet viewers for building up new webpage or even a weblog from start to end.

generic cialis capsules

I think this is among the such a lot important info for me.

And i am satisfied studying your article. But should remark on few common issues,

The web site style is wonderful, the articles is actually excellent : D.

Good process, cheers

canadian pharmacy generic cialis – cialis online pharmacy online tadalafil

Hey There. I found your blog using msn. This is an extremely well written article.

I will be sure to bookmark it and return to read more of your useful info.

Thanks for the post. I will certainly return.

tadalafil tablet 10mg price in india – cialis viagra comparison cheap generic tadalafil uk

viagra pills price in india

Hmm is anyone else encountering problems with the images

on this blog loading? I’m trying to determine if its a problem on my end or if it’s the blog.

Any responses would be greatly appreciated.

Turkcell kampanyalarından faydalanmak veya müşteri hizmetlerine bağlanmak için hemen adımıza tıklayın.

Hello there, I discovered your web site by means of Google while looking for a related subject,

your web site came up, it looks great. I have bookmarked it in my google bookmarks.

Hello there, simply became alert to your weblog via Google, and found that it is truly informative.

I’m gonna watch out for brussels. I’ll appreciate in case you proceed this in future.

Numerous other people will be benefited out of your writing.

Cheers!

Hi there! I’m at work surfing around your blog from my new iphone 4!

Just wanted to say I love reading through your blog and look forward to all your posts!

Keep up the excellent work!

Appreciating the persistence you put into your blog and in depth

information you provide. It’s nice to come across a blog every once in a

while that isn’t the same old rehashed information. Fantastic read!

I’ve bookmarked your site and I’m adding your RSS

feeds to my Google account.

Today, I went to the beachfront with my kids. I found a sea shell

and gave it to my 4 year old daughter and said “You can hear the ocean if you put this to your ear.” She put the shell to

her ear and screamed. There was a hermit crab inside and it pinched her

ear. She never wants to go back! LoL I know this is

entirely off topic but I had to tell someone!

Heya i am for the first time here. I found this board and I find It

really useful & it helped me out much. I hope to give something back

and aid others like you aided me.

Hi there i am kavin, its my first occasion to commenting anywhere, when i read this

post i thought i could also make comment due to this good piece of writing.

First off I would like to say superb blog! I had a quick question which I’d like to ask if you don’t mind.

I was curious to find out how you center yourself and

clear your mind prior to writing. I have had a hard time clearing my mind in getting my thoughts out.

I truly do enjoy writing however it just seems like the first 10 to 15 minutes are generally

wasted just trying to figure out how to begin. Any recommendations or hints?

Appreciate it!

Excellent blog you have here but I was wanting to know if you knew of any forums

that cover the same topics talked about in this article?

I’d really like to be a part of online community where

I can get responses from other experienced individuals

that share the same interest. If you have any suggestions, please let

me know. Cheers!

I need to to thank you for this wonderful read!! I definitely loved every little

bit of it. I’ve got you book-marked to look at new

things you post…

Very good information. Lucky me I ran across your website by chance

(stumbleupon). I’ve bookmarked it for later!

Hello, after reading this amazing paragraph i am also delighted to

share my know-how here with friends.

A person necessarily help to make severely posts I’d state.

That is the first time I frequented your website page

and thus far? I amazed with the analysis you made to create this

actual put up incredible. Great process!

Right here is the right web site for anyone who wants

to find out about this topic. You know so much its almost tough to

argue with you (not that I really will need to…HaHa).

You certainly put a new spin on a subject that has been discussed for years.

Excellent stuff, just great!

cost of ivermectin 3mg tablets – stromectol ireland stromectol xr

Link exchange is nothing else however it is

just placing the other person’s website link on your page at proper place and other person will also do same in favor of you.

Thanks to my father who stated to me about this website, this weblog is genuinely amazing.

This is my first time pay a visit at here and i am in fact pleassant

to read all at one place.

I think this is one of the most significant information for me.

And i am glad reading your article. But want to remark on few

general things, The site style is perfect, the articles is really nice

: D. Good job, cheers

Hey, I think your site might be having browser compatibility issues.

When I look at your blog site in Ie, it looks fine but when opening in Internet Explorer, it has

some overlapping. I just wanted to give you a quick heads up!

Other then that, wonderful blog!

whoah this weblog is magnificent i like reading your articles.

Stay up the good work! You already know, many

persons are searching around for this information, you could aid them

greatly.

I know this if off topic but I’m looking into starting my own blog and was wondering what all is needed to get set up?

I’m assuming having a blog like yours would cost

a pretty penny? I’m not very internet savvy so I’m not 100% certain. Any tips or advice would

be greatly appreciated. Appreciate it

stromectol uk buy – ivermectin 0.5 ivermectin price comparison

If you want to take much from this piece of writing then you have to apply such techniques to your won webpage.

I used to be able to find good advice from your

blog posts.

We absolutely love your blog and find almost all of your post’s to be exactly I’m

looking for. Do you offer guest writers to write content for yourself?

I wouldn’t mind composing a post or elaborating on some of the subjects you write related to here.

Again, awesome web log!

Good post! We are linking to this great post

on our site. Keep up the great writing.

At this time I am ready to do my breakfast, once

having my breakfast coming yet again to read additional news.

Heya i’m for the first time here. I found this board

and I find It really useful & it helped me out much.

I hope to give something back and help others like you aided me.

stromectol xl

generic ivermectin cream

I have read so many articles on the topic of the blogger lovers except this post is

actually a fastidious article, keep it up.

Asking questions are in fact fastidious thing if you are not understanding something completely, however

this piece of writing presents good understanding yet.

ivermectin rx

can i purchase prednisone without a prescription – order prednisone online safely generic prednisone

I visit everyday a few sites and websites to read content, however

this webpage gives feature based writing.

Way cool! Some extremely valid points! I appreciate you penning this write-up plus the rest of the site is also very

good.

obviously like your website but you need to check the spelling on quite a few of

your posts. Several of them are rife with spelling issues and I in finding it very bothersome to inform the truth on the

other hand I’ll surely come back again.

Great information. Lucky me I found your site by chance (stumbleupon).

I have saved as a favorite for later!

Appreciate this post. Will try it out.

I really like your blog.. very nice colors & theme.

Did you create this website yourself or did you

hire someone to do it for you? Plz respond as I’m looking to construct my own blog and would like to find out where

u got this from. thanks a lot

When I initially commented I clicked the “Notify me when new comments are added”

checkbox and now each time a comment is added I get four emails with the

same comment. Is there any way you can remove people from that service?

Cheers!

average cost of prednisone 20 mg – prednisone 105 online prednisone

each time i used to read smaller articles

or reviews which also clear their motive, and that is also happening

with this post which I am reading now.

ivermectin for sale

Hey there! This post could not be written any better!

Reading through this post reminds me of my previous room mate!

He always kept chatting about this. I will forward

this page to him. Pretty sure he will have

a good read. Thanks for sharing!

Hey there! I realize this is kind of off-topic but I had to ask.

Does running a well-established blog like yours require a large amount of work?

I am completely new to running a blog but I do

write in my journal everyday. I’d like to start a blog so I can share my experience and thoughts online.

Please let me know if you have any kind of recommendations

or tips for new aspiring bloggers. Appreciate it!

I’m impressed, I have to admit. Seldom do I come across a blog

that’s both educative and entertaining, and let me

tell you, you have hit the nail on the head. The problem is

something not enough men and women are speaking

intelligently about. Now i’m very happy I stumbled across this in my search for

something regarding this.

Right now it sounds like WordPress is the preferred

blogging platform out there right now. (from what I’ve read) Is that what you’re using on your blog?

This page truly has all the info I needed concerning this

subject and didn’t know who to ask.

Thanks for sharing your info. I really appreciate your efforts and I will be waiting for your further post thank you once

again.

Hello There. I found your blog using msn. This is an extremely well

written article. I’ll make sure to bookmark it and come back to read more of your useful information. Thanks for the post.

I’ll definitely return.

Ahaa, its pleasant discussion about this piece of writing at this place at this blog, I have read all that, so at this time

me also commenting here.

Hi, I do think this is a great website. I stumbledupon it 😉 I may revisit yet again since i have bookmarked it.

Money and freedom is the greatest way to change, may you be rich and continue to help others.

bookmarked!!, I like your site!

Hi there! Do you use Twitter? I’d like to follow you if

that would be ok. I’m undoubtedly enjoying your blog and look forward to new posts.

Simply desire to say your article is as astonishing. The clearness in your post is just cool and i can assume you are

an expert on this subject. Fine with your permission let me to grab your feed

to keep updated with forthcoming post. Thanks a million and please carry on the gratifying work.

ivermectin brand name

Appreciating the persistence you put into your site

and in depth information you provide. It’s good to come across a blog every once in a while that isn’t

the same outdated rehashed information. Great read! I’ve

saved your site and I’m including your RSS feeds to my Google

account.

Hi everyone, it’s my first pay a visit at this web site, and paragraph is truly

fruitful in favor of me, keep up posting such articles.

Howdy! I know this is kinda off topic but I’d figured I’d ask.

Would you be interested in exchanging links or maybe guest writing a blog article or vice-versa?

My site addresses a lot of the same subjects as yours and I feel we could greatly benefit from each other.

If you might be interested feel free to send me an email.

I look forward to hearing from you! Awesome blog by the way!

I’m really inspired with your writing talents as smartly as with

the structure to your weblog. Is this a paid topic or did you customize it yourself?

Either way stay up the nice quality writing, it’s rare to look a nice blog like this one today..

Wonderful goods from you, man. I have understand your stuff previous to and you’re just extremely great.

I actually like what you’ve acquired here, certainly like what you are saying and the way in which you say it.

You make it entertaining and you still care for

to keep it sensible. I can not wait to read much more from you.

This is actually a wonderful site.

I was able to find good information from your content.

Unquestionably believe that which you said. Your favorite justification seemed

to be on the internet the easiest thing to be aware of.

I say to you, I definitely get annoyed while people think about worries that they plainly

do not know about. You managed to hit the nail upon the top

and also defined out the whole thing without having side-effects , people could take a signal.

Will likely be back to get more. Thanks

ivermectin 4

modafinil and weight loss – modapls.com modafinil adhd

Hello, after reading this amazing article i am also

happy to share my knowledge here with colleagues.

Write more, thats all I have to say. Literally, it seems as

though you relied on the video to make your point. You obviously

know what youre talking about, why throw away your intelligence on just posting videos to your weblog when you could be giving us something enlightening to read?

Hello to every single one, it’s really a pleasant for me to go to see this website,

it contains useful Information.

Hi there i am kavin, its my first occasion to commenting anyplace, when i read

this article i thought i could also create comment due to this brilliant paragraph.

Howdy! This post couldn’t be written any better! Reading this post reminds me of my good old room mate!

He always kept chatting about this. I will forward this page to him.

Fairly certain he will have a good read. Many thanks for sharing!

I constantly spent my half an hour to read this weblog’s posts every day along with a cup of coffee.

Hey there! Someone in my Facebook group shared this

site with us so I came to check it out. I’m definitely

loving the information. I’m book-marking and will be tweeting this to my followers!

Excellent blog and outstanding style and design.

Heya exceptional blog! Does running a blog such as this take a great deal of work?

I’ve no expertise in programming but I had been hoping to

start my own blog in the near future. Anyhow, if

you have any suggestions or tips for new blog owners please share.

I understand this is off topic however I simply had to ask.

Many thanks!

Hello there! This is my 1st comment here so I just wanted

to give a quick shout out and tell you I genuinely enjoy

reading through your articles. Can you suggest any

other blogs/websites/forums that deal with the same subjects?

Thanks a ton!

modafinil side effects – modafinil and alcohol modafinil 100mg

What you said made a bunch of sense. But, what about this?

what if you were to write a awesome title? I ain’t saying your information isn’t solid, but what if you added a title

that grabbed a person’s attention? I mean Your Portfolio is Not

as Diversified as You Think | RetirementFinance.Org is a little vanilla.

You might look at Yahoo’s home page and watch how they create post headlines to get

viewers interested. You might add a video or

a picture or two to get people interested about what you’ve got to say.

Just my opinion, it might make your posts a little livelier.

cost of ivermectin 1% cream

I was able to find good information from your blog articles.

Everything is very open with a very clear explanation of the issues.

It was definitely informative. Your website is very helpful.

Thank you for sharing!

I am regular visitor, how are you everybody? This paragraph posted at this site

is in fact pleasant.

great points altogether, you just won a new reader. What might you

recommend in regards to your put up that you simply made a few days in the past?

Any positive?

Wow that was unusual. I just wrote an extremely long comment but after I clicked submit my comment didn’t appear.

Grrrr… well I’m not writing all that over again. Anyway, just wanted to say excellent blog!

Wonderful, what a website it is! This webpage gives useful

facts to us, keep it up.

It’s an remarkable post for all the internet people;

they will take advantage from it I am sure.

Remarkable! Its in fact amazing piece of writing, I have got much clear

idea about from this post.

stromectol 0.1

Its like you read my mind! You appear to know a

lot about this, like you wrote the book in it or something.

I think that you could do with some pics to drive the message home

a little bit, but instead of that, this is great blog.

A great read. I’ll certainly be back.

Please let me know if you’re looking for a author for your site.

You have some really good posts and I feel I would be a good asset.

If you ever want to take some of the load off, I’d

absolutely love to write some material for your blog in exchange for a link back to mine.

Please send me an email if interested. Thank you!

Hi there mates, nice paragraph and good arguments commented at this place, I am genuinely

enjoying by these.

Hi there, yes this paragraph is genuinely pleasant

and I have learned lot of things from it on the topic of blogging.

thanks.

Wonderful post however I was wondering if you could write a

litte more on this topic? I’d be very grateful if you could elaborate a little bit further.

Thanks!

whoah this blog is excellent i like studying your articles.

Stay up the great work! You already know, many people are hunting around for

this info, you could help them greatly.

My brother recommended I would possibly like this web site.

He used to be entirely right. This put up actually made my day.

You can not imagine simply how so much time I had spent

for this info! Thanks!

ivermectin online

Asking questions are actually pleasant thing if you are not understanding

anything fully, except this article offers pleasant understanding even.

you’re in reality a just right webmaster. The website loading speed is amazing.

It sort of feels that you’re doing any distinctive trick.

Furthermore, The contents are masterpiece. you’ve done a fantastic job on this matter!

Hey there! I’m at work surfing around your blog from my new iphone!

Just wanted to say I love reading your blog and look forward to all your posts!

Keep up the outstanding work!

Hi there Dear, are you genuinely visiting this website regularly,

if so afterward you will definitely take fastidious know-how.

I am in fact grateful to the holder of this website who has shared this

great article at at this place.

ivermectin otc

order zithromax 250mg – citromax generic zithromax over the counter

Hello would you mind letting me know which webhost you’re working with?

I’ve loaded your blog in 3 different web browsers and I must say this blog loads a lot faster then most.

Can you suggest a good hosting provider at a fair price?

Thanks, I appreciate it!

I was recommended this web site by my cousin. I’m not sure whether this post is written by him as nobody else

know such detailed about my problem. You are amazing! Thanks!

Hello this is somewhat of off topic but I was wondering if blogs use

WYSIWYG editors or if you have to manually code with HTML.

I’m starting a blog soon but have no coding skills so I wanted to get advice from someone with experience.

Any help would be enormously appreciated!