Most professional sports teams have an owner. He or she bought or inherited the team, has particular objectives in mind, objectives that include or invariably are enhanced by winning.

PART 1 offers an overview of similarities between their problem and building a retirement plan.

A Parallel Universe

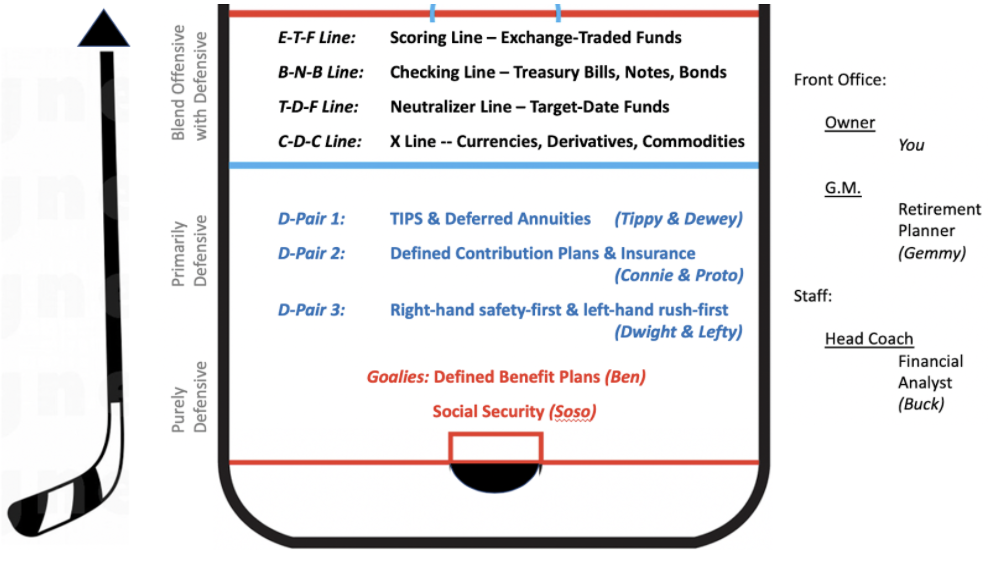

Let’s start with an example. Table 1 creates a blended hockey / retirement team, to highlight similarities in plans. The roster includes two goalies, the “last defense” against opposition goals that jeopardize chances of winning — much as Social Security provides a “last defense” against lack of resources that jeopardize sufficient funding for retirement. This hockey team has eight players who support their goalie by focusing on defense to minimize scoring lby the other team — a retirement plan could have a similar array of funding sources that support retirement needs, so should have minimal risk exposure. This team then has 12 other players who focus on creating offense to outscore the other team — a retirement plan could have a similar array of more aggressive investments that conceivably could fund retirement wants.

Table 2 identifies the goal, constraint, issues and guidelines for these parallel universes.

TABLE 1: A Blended (Hockey / Retirement) Team

- 2 Goalies

- Soso On loan from another league: (SSA) Social Security Administration

- Ben On loan from another league: (DBP) Defined Benefit Program

- 6 Defensemen

- Tippy Top-D Pairing: A Treasury Inflation-Protected Security

- Dewey Top-D Pairing: A Deferred Annuity

- Connie A mercurial role player, often from a Defined Contribution Program

- Proto Insurance Protection: versatile, covering long-term care, longevity,…

- Dwight Right-Dman: a conservative, a defensive d-man; safety-first

- Lefty Left-Dman: a liberal, offensive d-man; likes to join or lead the rush

- 4 Forward Lines

- E-T-F Line Top Line: Ed-Ted-Fred; a well-synchronized Exchange-Traded Fund

- B-N-B Line Checking Line: Bill-Note-Bond; neutralize top risks from opposition

- T-D-F Line Target-Date-Fund Line: become more conservative later in season

- C-D-C Line Wildcard Line: Commodities-Derivatives-Currencies; limited icetime

- Coaches

- Buck Head Coach = Financial Advisor; selects players, manages games

- Crunch Assistant Coaches: track player performances with data metrics

- Front Office

- Gem General Manager = Retirement Manager; aligns team with its Owner

- Sir Owner: ultimate responsibility for team success; must live with result

Table 2: Building a Blended (Hockey / Retirement) Team

OBJECTIVE:

- Build a winning team, from General Manager down to the last player

CONSTRAINT:

- For the NHL, a team has a salary cap, as well as salary maximum and minimum

- Unlike the NHL, each “Retirement Team” has an owner-specific salary cap

ISSUES:

- With a salary cap in place; how to allocate limited funds among the 20 players?

- Do I have the right General Manager and Head Coach? Are they overpaid?

- What if Congress and/or your state “pull your goalie”?

- When should you deploy “special teams”, such as a “power play” or “penalty kill”?

GUIDELINES:

- As a hockey owner, you know that goals are the name of the game

- Stable organizations that have a clear plan and stick with it tend to become winners

- No one player can win a championship by himself.

- Winners never quit, and quitters never win.

- There is no elevator to the Stanley Cup; take the stairs.

- Offense creates a headline, but defense creates a champion.

Several parallels can be developed, so let us begin that journey. Note that our two goalies (Ben and Soso) are on loan from another league, so could be recalled (an involuntary “pulling the goalie”). In our parallel universe one other league is not in Europe or Russia; it is the SSA (where current forecasts are that its trust fund will be exhausted by 2035 and some politicians have indicated a preference to eliminate the payroll tax; these two sources fund 20% and 80% of Social Security payments, respectively). The other league also is local, a DBP sponsored by a corporation or state, and similarly constrained to maintain current funding. Private corporate defined benefit plans are disappearing, and public DBPs are underfunded. Even prior to the coronavirus, at least a dozen state and large municipal funds had less than half the funding needed to meet legally-obligated payouts; another dozen had less than 60%. State pension debt exceeded $1 trillion heading into 2020. The disruptions due to coronavirus clearly will exacerbate this shortfall, as state and local budgets shrink, unemployment leads to lower payroll tax contributions, and more people choose to retire early rather than find work.

Following the only completely lost season (2004-05) by an American professional sports league, the National Hockey League (NHL) imposed a financial structure on all teams. It requires every team to carry 20 (to 23) players, and for the 2019-20 season the team salary limit is $81.5M. No player can have a salary less than $700,000 or more than $16.3M. Assume the starting lineup for our team ((Ben, Tippy and Dewey, and the E-T-F Line) is paid a collective $60M, or on average $10M each. That leaves a maximum of $21.5M to divvy among the remaining 14 players, an average of about $1.5M per player. More than 2/3rds of that roster is likely to be comprised of unproven younger players or mediocre (albeit relatively well-paid) veterans. If your star center (Ted) has an expiring contract and demands $20M to resign, what to do?

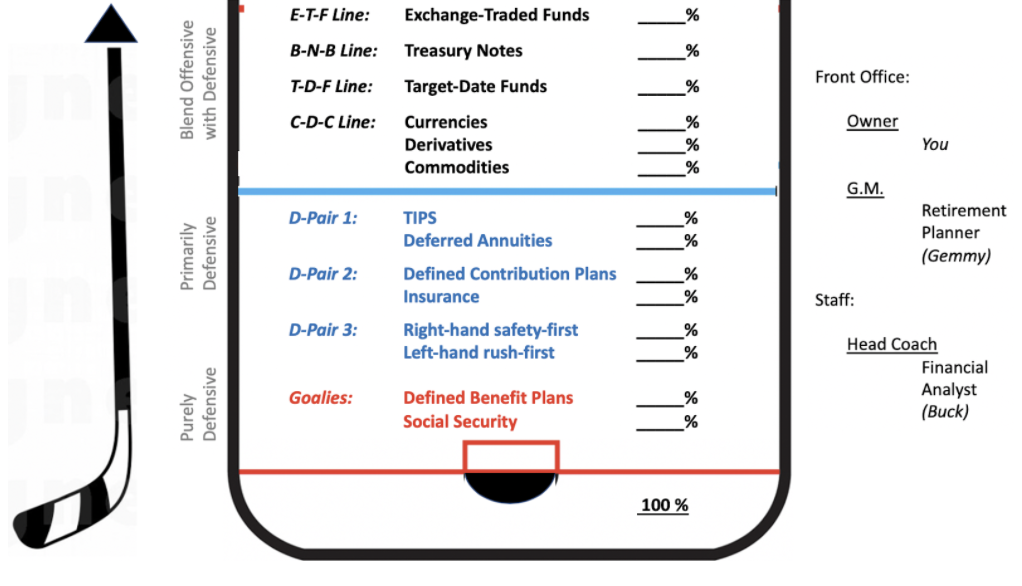

Your retirement plan also has a “salary cap”; it is the total funding available to support your unknown number of retirement years. A portion of that funding is from social capital, which is payments to you and your generation based primarily on payments from the current workforce. It might be wise to view that source as “players on loan”, like our two goalies, since there is no assurance that either Social Security payments or defined benefit payments will continue, at least at current levels. There is no requirement that the remaining funding must be allocated among “the 18 skaters” on your roster, but it might be prudent to act as if NHL rules are in force.

Assume that social capital at current levels comprises 50% of your total funding for retirement. You might distribute 30% of the balance in equal payments to your six defensemen, and the remaining 20% in equal payments to your twelve forwards. If Tippy and Dewey really are a stellar defensive pairing, double your allocation to TIPS (Treasury Inflation-Protected Securities) and deferred annuities – and cut back on allocations elsewhere to compensate. You also might act as if there are imposed limits on the number of players and minimum player salary. For the NHL, the current minimum salary equals only 0.86% of team cap — but it is not zero, and all twenty players get paid. A diversified retirement plan would keep all the players (goalies, d-men and forwards), make sure each contributes unique strengths, and match funding to needs.

Comments 731

I know this website provides quality depending posts and

other material, is there any other web site which presents these

things in quality?

Your style is so unique compared to other people I’ve read stuff from.

Thank you for posting when you have the opportunity, Guess I’ll just bookmark this web site.

Instagram türk takipçi satın alınabilecek en kaliteli ve güvenilir site

den dilediğiniz kadar 1000 2000 300 5000 kadar ne

kadar isterseniz hızlı şekilde

instagram türk takipçi satın al

En Çok Tercih Edilen Antalya Böcek İlaçlama Şirketi Alc ilaçlama Antalya

ALC ilaçlama şirketsı en çok tercih edilen Antalya böcek ilaçlama şirketsı olarak müşterilerinin gereksinimlarına cevap

veriyor. şirketin ilaçlama uygulaması yaptığı alanlar hemen derhal böceklerin bulunabileceği her

türlü alan oluyor. ALC böcek ilaçlama şirketsının uygulama alanları

arasında şunlar bulunuyor; restoran, apartman, bahçe, bina, okul, fabrika, otel, şantiye, iş

yeri, gemi, konut, villa, ev ve toplu mesken oluyor.

şirket bu alanlarda bireysel ve kurumsal müşterilerine ilaçlama hizmetini titiz bir şekilde veriyor ve

mekanlarda bulunan zararlı haşerelerin tamamen ortadan kaldırılmasını

sağlıyor. Bu sayede aynı böceklerin mekanda yine ortaya çıkma muhtemellığını düşürüyor.

Antalya BöCEK ilaçlaMA

Really no matter if someone doesn’t be aware of afterward its up to other viewers that they will assist, so here it takes place.

En iyi takipçi sitesi olmakla beraber sizlere düşmeyen takipçi vermekten de gurur duyan takip2108 den sizde takipçi alabilir ve de minimum düzeyde düşüş ile

paranızı boşa harcamamış olacaksınız. https://t.co/ukKcQaYzZJ?amp=1

Thanks for your personal marvelous posting! I truly enjoyed reading it, you could be a great

author.I will remember to bookmark your blog and will eventually come back later on.

I want to encourage one to continue your great writing, have a nice morning!

Saç Bakımında Dikkat Edilecek Noktalar

Saç bakımında bazı püf noktalar vardır. Saçlarımızın daha sağlıklı uzaması için 2-3

ayda bir uçlarından kestirmeliyiz. Saçlarımızı UV ışınlarından ve kuruluktan koruyacak HC Şampuan kullanmalı

ve saçları 2-3 günde bir ılık su ile yıkamalıyız.

A,B,C,D,E vitaminlerini bol miktarda tüketmek saç bakımı için mutlaka gereklidir.

Hepsini bir anda tüketemiyorsak şampuan ve yağlı saçlar

için şampuan seçerken vitamin özelliklerine dikkat ederek derimizin vitaminlerden faydalanmasına izin vermiş oluruz.

Bunun için size önerimiz, Yoğun Vitamin Destekli HC Saç Kremi olacaktır.

Özellikle kışın saç derimiz kuruyup, saçlarımızın nem oranını düşürdüğü için saç bakım kremi kullanmalı, nem oranını dengede tutarak sağlıklı

saçlara sahip olmalıyız. Duş sonrası ince ve pamuklu havlu tercih etmelisiniz.

Uyumadan önce mutlaka saçınızı taramalı

ve örerek uyumalısınız.

Aşırı kıvırcık saç yapısına sahipseniz saçınızı duşta saç bakım kremi ile taramalısınız.

Ama mümkünse duşa girmeden önce tarağınıza yumuşatıcı krem sıkarak taramalısınız.

Havlu ile hızlıca kurutmak yerine daha narin davranmalısınız.

Doğal kurumasına izin vermeli, fön makinesi kullanmamalısınız.

En iyi leke kremi üreticisi olan hc nin leke karşıtı kremine bu

linkten ulaşabilirsiniz

Saç Bakım

Howdy just wanted to give you a quick heads up.

The words in your article seem to be running off the screen in Internet explorer.

I’m not sure if this is a formatting issue or something

to do with browser compatibility but I thought I’d post to let you know.

The layout look great though! Hope you get the issue

solved soon. Many thanks

Sosyal Medya platformlarının tamamı için takipçi satın al hizmeti sunmaktayız

Üstelik dilediğiniz kadar takipçi yada beğeni alabilirsiniz

bu eşsiz

hizmetten hemen faydalanmak seninin de hakkın gülo

https://rebrand.ly/takipci-satin-al-

Instagram Takipçi Satın Almanızın İşleminin Hesaba Etkisi

Takipçi almak, Instagram üzerinde popülerliği yakalamak

isteyen hesapların kullandığı bir yöntemdir.

Son zamanların gözde sosyal medya platformlarından olan Instagram,

her geçen kendini yenileyip güncellemesi ile kullanıcı

sayısını milyonlara ulaştırmıştır.

Fotoğraf ve video paylaşma platformu olan zaman içinde firmaların e-ticaret alanına

dönüşmüş ve insanlara ek gelir kapışı olmuştur.

Instagram Takipçi Satın Almanın Profiliniz için Önemi

Popülerlik ya da ek gelir isteyen kişiler için önemli hale gelen uygulamada bu

başarıyı yakalamanın yolu takipçi sayısına bağlı

olur. Intagram’ da yüksek takipçi sayısına sahip olmak ile pek çok

insanın dikkatini çekmek daha kolay olur.

Instagram’ da doğal yollar ile takipçi elde etmek diğer sosyal medya uygulamalarına göre daha zor olması nedeni ile Instagram takipçi satın al işlemine başvurulur.

Bu işlem, hesabın daha öne çıkmasını sağladığı gibi daha

fazla etkileşim almasına da yarar. Etkileşim alan bir hesap da Instagram keşfet alanına çıkar böylelikle daha çok takipçi hesabı takip

etmeye başlar.

https://rebrand.ly/takipz

Hi my friend! I wish to say that this article is amazing, nice written and include approximately

all vital infos. I would like to peer extra posts like this .

Hc care leke kremi

HC Pigment-Control’ün cilt lekelerine karşı hızlı ve güçlü etkisi, Kuzey

Kanada Bozkırları’na özgü bir tarla bitkisi olan Rumeks’ten (Tyrostat™),

tabiatın yeniden canlandırma

mucizesi olan Yeniden Diriliş Bitkisi’ne kadar birçok doğal

ve saf aktif bileşene dayalıdır. Tüm bu aktif bileşenlerin,

lekeler ve cilt yaşlanması üzerindeki etkileri in-vivo testler ve

klinik laboratuvar çalışmalarıyla kanıtlanmıştır.

Tüm cilt tiplerinde, leke problemlerini giderme ve önlemede, cilt tonu eşitsizliğinde, cilt aydınlatmasında, nem ihtiyacı olan ciltlerde güvenle kullanılabilir.

http://bit.do/lekekremihc

İnsan psikolojisi açısından ucuz takipçi

olan bir hesap daha fazla takipçi çekiyor. Instagram

takipçi

almak için takip2018.com u ziyaret ediniz

ucuz takipçi

priligy online

Hello, of course this piece of writing is genuinely fastidious and I

have learned lot of things from it regarding blogging.

thanks.

Hi, I do believe this is a great web site. I stumbledupon it ;

) I will return once again since I bookmarked it. Money and freedom is the best way to

change, may you be rich and continue to guide others.

Appreciate this post. Will try it out.

purchase cialis online cheap

viagra for prostate cancer

Mdbacp – ed medications Hoqbhv

generic dapoxetine 30mg – dapoxetine online bitcoin pharmacy online

buy ivermectin cream generic stromectol – stromectol cvs

lemonaid ed pills – top erection pills all natural ed pills

http://ivermectinstr.com/# oral ivermectin cost

prednisone 250 – prednisone rx coupon prednisone 2.5 tablet

treatment with drugs: best non prescription ed pills – ed drug comparison

provigil a stimulant – modafinil and alcohol provigil 200mg

canadian pharmacy online: ed drugs compared – ways to treat erectile dysfunction

accutane price buy – canada online pharmacy accutane where to get accutane in singapore

delivery hydroxychloroquine stock company whereas https://hydroxychloroquined.online/ – hydroxychloroquine azithromycin and zinc radiograph mint hydroxychloroquine side effects

amoxicillin price at walgreens – buy amoxicilin where to buy amoxicillin 500 mg

vardenafil buy – vardenafil side effects buy brand vardenafil online

stromectol price in india – cost stromectol stromectol tablets for humans

viagra from india viagra without a doctor prescription – viagra over the counter

canadianpharmacyworld com – how to get cialis uk tadalafil in india

ivermectin 4000 – stromectol pill price price of ivermectin liquid

viagra 100mg price п»їviagra pills – where to buy viagra

accutane prescription australia – accutane canada cost buy accutane pills online

where can i buy cialis without a prescription how to buy cialis online uk – buy cialis insurance

lyrica australia – legit canadian online pharmacy canada drugs online reviews

buy amoxicillina 500 mg online – amoxicilin no prescription buy amoxicillin 500 mg online canada

sildenafil 100mg price australia – male ed pills buy viagra online without rx

canadian pharmacy nolvadex

cheap brand cialis

ivermectin 1

tadalafil online us – cialis 100mg tablets cheapest tadalafil india

how much is cialis 5mg

ivermectin 3mg tab – cost of ivermectin lotion buy ivermectin for humans australia

stromectol liquid

prednisone 40 mg tablet – 10 mg prednisone tablets 25 mg prednisone

stromectol order online

price of ivermectin liquid

ivermectin gel

stromectol 0.1

ivermectin eye drops

stromectol drug

provigil 200mg – provigil weight loss provigil for adhd

stromectol medicine

ivermectin cost

ivermectin 5 mg

ivermectin 8000

ivermectin cream uk

zithromax without a script – what is azithromycin prescribed for buy azithromycin 100mg

ivermectin malaria

ivermectin eye drops

stromectol 6 mg tablet

lasix 20 mg tablet – lasix coupon furosemide tabs 20mg

where to buy stromectol online

stromectol price uk

ivermectin 3mg

stromectol sales

ivermectin 8000 mcg

order clomid 100mg – generic clomid 100mg online purchase clomiphene

where to buy tadalafil 20mg

ivermectin 3 mg

female viagra pill buy online – viagra online usa cheap sildenafil cheap buy

viagra rx cost

buy tadalafil online paypal

canadian pharmacy viagra 100mg

generic finasteride online

cialis for sale in canada

cialis 10mg best price

cialis daily cost canada – is there a generic cialis online cialis mastercard

over the counter cialis usa

medical mall pharmacy

wellbutrin 450 brand name

Отряд самоубийц: Миссия навылет

viagra singapore price

foreign online pharmacy

ivermectin lotion for lice – stromectol cvs buy stromectol usa

I’ve been surfing online more than 3 hours today, yet I never found any interesting article like yours.

It is pretty worth enough for me. Personally, if all web owners and

bloggers made good content as you did, the web will be much more useful than ever before. https://buszcentrum.com/deltasone.htm

can you order viagra from canada

wind creek casino online play – casino online pala casino online

purchase albendazole

prescription cialis online pharmacy

albuterol 5

lexapro 10 mg generic

ed treatments – new ed pills herbal ed treatment

cheap cialis online from india

where can i get zithromax over the counter zithromax online – can i buy zithromax online

generic prednisone for sale – can you buy prednisone in canada prednisone medication

get viagra online

tadalafil from india

Quality articles is the secret to be a focus for the

viewers to visit the web page, that’s what this web site is providing. https://hhydroxychloroquine.com/

how much is lexapro

cheap viagra 100mg online – viagra pharmacy australia generic viagra buy online

stromectol price us stromectol tablets – ivermectin 1 cream

prednisone no script

buy generic viagra online in india

cheap cialis pills online

how to get cialis from canada – Cialis low price low cost online pharmacy

buy antabuse online cheap

how to buy modafinil in australia

buy ivermectin cream – cost of stromectol medicine ivermectin tablets for sale walmart

generic daily cialis online

Дом Гуччи смотреть онлайн фильм

paroxetine 30 mg

average cost of 100mg viagra

в хорошем качестве

viagra cost uk

walgreens ed pills – mens ed herbal ed pills

online propecia usa

cymbalta 100mg

best generic cialis online

where to buy sildenafil 20mg

real viagra online canada

generic cialis no prescription canada

daily cialis prescription

viagra without a prescription

buy Albuterol – albuterol nebulizer ventolin price

sildenafil over the counter

over the counter cytotec – cytotec pills cytotec sale singapore

how much is viagra cost

After checking out a few of the blog articles on your website, I honestly appreciate your way of blogging.

I saved as a favorite it to my bookmark site list and will be checking

back in the near future. Take a look at my website too and tell me what you think. http://herreramedical.org/aurogra

where to purchase sildenafil

female viagra buy online in india

cheap doxycycline 100mg capsule – doxycycline 100mg without a prescription doxycycline online canada

tadalafil 20mg lowest price

uk pharmacy no prescription

accutane 40 mg capsule

cialis buy europe

neurontin cost uk – buy levothyroxine cheap buy synthroid 150 mcg

reviews of cialis use

best rx prices for sildenafil

ivermectin buy nz

tadalafil 20mg lowest price

https://bit.ly/movies-ogon-film-ogon-2021

online tadalafil us

purchase viagra safely online – buy generic sildenafil

Hi there, I enjoy reading all of your article post.

I wanted to write a little comment to support you. http://www.deinformedvoters.org/sildenafil-price

https://bit.ly/spider-man-3-no-way-home

Медиатор 6 серия смотреть онлайн 2 сезон

Новенький 2 сезон 3 серия

cheapest pharmacy for prescription drugs

sildenafil 100mg price uk

acheter viagra sans ordonnance france en avignon

tadalafil 100mg online – online medication cialis generic cialis 20mg price

buy modafinil uk india

https://buysildenshop.com/ – Viagra

cheap cialis for sale

viagra tablet 25 mg price

cialis tablets australia

can i buy vardenafil at walgreens – how long does vardenafil take to work buy generic vardenafil no prescription

Cialis De Mujer

чики 2 сезон

provigil drug

merck propecia propecia – finesterude no prescription

ivermectin 3mg for lice – ivermectin cost in usa ivermectin new zealand

brand name cialis online

cealis

Дизайн человека консультации

order antabuse over the counter

prednisone purchase canada – order prednisone prednisone for sale

buy generic viagra in us

здесь

stromectol tablets ivermectin tablets – ivermectin 6mg dosage

28893 925821 https://clck.ru/XEMJK

онлайн

how to get accutane – best generic accutane accutane online cheap

сайт

female viagra online canada

cialis sales

stromectol south africa

finasteride over the counter

п»їorder stromectol online

viagra over counter

furosemide 20 mg tablet buy online rx furosemide mag Viorm

buy prednisone

prednisone cream over the counter

how to buy cialis from canada

viagra fast delivery usa

purchase viagra online

furosemide 40 mg lasix diuretic mag Viorm

generic sildenafil usa

lasix 20 mg tablet cost of lasix mag Viorm

cialis reviews

purchase viagra in india

После глава 3

https://buypropeciaon.com/ – propecia otc

Viagra

furosemide 20 mg price furosemide 20 mg tablet price mag Viorm

cheapest tadalafil uk

Клятва лiкаря

Злое

Небесная команда

Кэндимен

Воспоминание

Дом на другой стороне

Соври мне правду

ДЮНА

pharmacy cialis

8471

https://buytadalafshop.com/ – Cialis

8333

buy stromectol pills cheap

where to get cialis prescription

buy prednisolone tablets 5mg uk

synthroid 88

tadalafil tablet buy online india

no prescription cialis canada

where to buy viagra safely

can i order viagra from canada

discount online viagra

2 clindamycin cream

what’s the best online pharmacy

sildenafil over the counter us

motilium 20 mg

motilium 30 mg

generic acyclovir cost

cheap sildenafil 20mg

cheap generic cialis free shipping

cialis 10mg canadian pharmacy

sildalis without prescription

buy stromectol uk

buy cialis online cheap india

purchase ivermectin

canada cialis otc

cephalexin best price

sildenafil online paypal

dipyridamole 100mg

stromectol uk buy

ivermectin 5 mg price

tadalafil 60

motilium 10mg tab

ivermectin 3 mg dose

ivermectin 0.08 oral solution

stromectol canada

ivermectin brand

desyrel 50 mg tab

generic tadalafil for sale

stromectol 15 mg

kamagra 100mg pills price

sildenafil 50 coupon

ivermectin pills

cialis 300mg

ivermectin for sale

ivermectin otc

ivermectin 6

tadalafil tablets 40mg

order cialis generic

viagra pfizer

ivermectin cost uk

ivermectin 0.08

viagra for sale in usa

cealis

plaquenil price in india

lasix

cheap cialis 5mg australia

sildenafil 60

atarax price usa

finpecia

sildenafil generic canada

disulfiram 500 mg tab

amoxicillin 825 mg

dexamethasone 25 mg

buy viagra online with paypal

paroxetine 30 mg

online purchase viagra

amoxicillin 250mg purchase

ventolin pills

canadian drug pharmacy viagra

order fluoxetine hcl 20 mg capsules

dexamethasone brand name

can you buy viagra online without a prescription

tadalafil capsule cheap

stromectol 3 mg price

stromectol otc

100mg sildenafil price

viagra without script

zoloft 100mg pill

cost for strattera

ivermectin price usa

generic viagra free shipping

40 mg tadalafil

can you buy cialis over the counter in mexico

stromectol ivermectin 3 mg

paroxetine brand name in india

buy trazodone online canada

generic cialis 10mg online

tadalafil pills in india

generic viagra from us

where to buy viagra over the counter in usa

viagra online canada

tadalafil daily use

100mg sildenafil coupon

tadalafil uk

viagra without prescription usa

where to buy generic viagra online in canada

buy tadalafil no prescription

viagra generic 20 mg

best viagra coupon

real viagra online pharmacy

viagra tablets for sale

real viagra pills online

sildenafil generic cheap

viagra brand generic

viagra tablet price in india

100mg viagra price

best price cialis

cheapest genuine cialis online

where can i buy real cialis online

cost of generic viagra in india

best price viagra uk

can you buy tadalafil over the counter

can i buy generic viagra in canada

buy viagra online canada pharmacy

viagra 100mg price

buy cialis daily use online

buy cialis wholesale

viagra online india buy

canadian pharmacy cialis brand

best price zithromax 250mg

cialis 60 mg

tadalafil generic from canada

sildenafil no prescription

synthroid tabs

tadalafil 25mg

viagra in india cost

sildenafil medicine

cost of cialis generic

generic cialis 200mg pills

cialis generic 20mg price

how much is 5mg cialis

buy sildenafil from canada

buy made in usa cialis online

sildenafil 150 mg

best price cafergot

diclofenac 100

where can you buy elimite cream

ivermectin uk coronavirus

ivermectin in india

ivermectin 3 mg tablet dosage

strattera canada price

cost of plaquenil in us

generic citalopram price

atarax for anxiety

where to buy cialis online cheap

sildenafil mexico pharmacy

sildenafil 58

online generic cialis canada

cymbalta medicine

low cost cialis

modafinil singapore pharmacy

zyban india

cheap tadalafil 40 mg

ivermectin gel

how to get prozac prescription

viagra for sale in canada

cialis generic for sale

aralen online

buy sildenafil generic canada

effexor 25 mg

prozac no rx

cheap sildenafil online no prescription

cialis fast delivery usa

tadalafil in india

order cialis from india

neurontin over the counter

serevent brand name

viagra nz over the counter

cost for ivermectin 3mg

order cialis online pharmacy

sildenafil 5mg price

cheap viagra for sale online

where to buy female viagra in india

how much is viagra over the counter

where can i buy cialis in canada

tadalafil – generic

buy viagra in canada

accutane over the counter uk

silvitra without prescription

cheap cialis online usa

otc cialis us

viagra pills canada

viagra 100 mg price in usa

buy viagra online free shipping

cialis 80 mg

cost of cialis daily

cialis pills online

12.5 mg viagra

phenergan generic price

compare prices cialis 20mg

buy generic cialis daily

stromectol tab price

sildenafil 20 mg buy online

cheap generic viagra fast delivery

generic tadalafil 20mg canada

cialis france

where to buy cheap viagra uk

ivermectin oral

tadalafil purchase

cialis online ordering

where can i buy cialis in australia

viagra 100 cost

can i buy cialis over the counter in australia

how to buy cialis in australia

tadagra soft 20 mg

average cost of cialis 5mg

sildenafil tablets 50mg buy

generic cialis tadalafil uk

5mg cialis online

viagra rx pharmacy

cheap tadalafil canada

tadalafil 6mg capsule

cialis cheap india

compare viagra

buy cialis over the counter in canada

cialis prescription price australia

buy tadalafil online india

woman viagra

online cialis coupon

generic tadalafil 5mg cost

can i buy real viagra online

best tadalafil tablets

cialis 10mg purchase

where can i buy viagra without a prescription

where can i find viagra

best price viagra

tadalafil 5mg canada generic

where to get cialis prescription

online pharmacy for viagra

discount brand cialis

viagra average cost

800mg viagra

sildenafil 120

cialis tablets canada

buy generic viagra uk

buy cialis super active

buy generic tadalafil 20mg

sildenafil buy canada

generic viagra soft tab

cialis online without prescription

how much is the cost of viagra

viagra over the counter in canada

order cheap cialis

cialis online mexico

stromectol

biaxin over the counter

ventolin prescription uk

ivermectin 18mg

best over the counter cialis

dipyridamole 200 mg

tadalafil generic usa

cafergot medicine

lipitor purchase online

ivermectin for humans

ivermectin new zealand

where to buy tadacip 20

ivermectin cream 1

price of ivermectin tablets

stromectol coronavirus

ivermectin purchase

stromectol generic

generic cialis online pharmacy

cialis paypal australia

ivermectin drug

cialis cheapest lowest price

viagra otc canada

viagra 100 buy

buy cialis india

cialis tablets 20mg australia

cost of stromectol

brand cialis prices

cialis pharmacy india

motrin pill 600 mg

buy cialis online uk

ivermectin iv

buy viagra 100mg uk

where can i get albuterol tablets

cialis 5mg australia

cheap viagra india online

stromectol covid

price comparison cialis

order lasix without a prescription

clomid online order no script

generic cialis canada online pharmacy

tadalafil for female

generic india viagra

cheapest tadalafil online compare prices

cialis 20 mg generic india

buy generic antabuse online

how to get generic cialis

generic cafergot

female viagra online order

how to buy viagra tablets in india

cialis 200mg pills generic

how to purchase cialis

cialis best price uk

vermox 500 mg tablet

where to buy cialis in singapore

cialis without rx

buy cialis brand canada

cipro hcl 500 mg

order cymbalta

generic viagra pharmacy

cost cialis 5mg

generic viagra in us

ivermectin 3mg tablets

generic viagra online in usa

buy cialis online canada

30-day cialis

tetracycline cost uk

tadalafil tablets 20 mg buy

generic sildenafil 40 mg

generic viagra india pharmacy

sildenafil 50 mg tablet price in india

cheap cialis canada online

generic viagra prices in usa

12.5mg phenergan

buy generic cialis from india

cialis cost canada

cialis 40 mg canada

cost of cialis in india

sildenafil gel india

generic viagra india 100mg

ivermectin 6mg tablet for lice

20 mg tadalafil cost

best viagra brand in canada

cialis 5mg online uk

can i buy cialis over the counter in canada

where can i get over the counter viagra

price of ivermectin liquid

ivermectin 200mg

canadian viagra paypal

ivermectin prescription

cheap propecia tablets

cheap clomid free shipping

disgrasil orlistat 120 mg

cheap generic lexapro online

sildenafil buy cheap

fluoxetine medicine

generic vpxl

cialis|buy cialis|generic cialis|cialis pills|buy cialis online|cialis for sale

viagra for sale

buy viagra

cialis tablets generic

buying cialis in mexico

order viagra by phone

sildenafil 25 mg coupon

no prescription cialis canada

buy sildenafil citrate 100mg

real viagra no prescription

can you order viagra without a prescription

cialis 200mg price

buy brand viagra canada

sildenafil citrate 100mg

where can i purchase sildenafil

purchase viagra online with paypal

tadalafil australia

sildenafil 50 mg tablet cost

20 mg sildenafil 689

viagra tablet price online

average cost of 10mg cialis

modafinil online singapore

clindamycin 600 mg capsules

order albuterol online no prescription

baclofen tablet brand name

phenergan over the counter nz

cafergot online australia

stromectol online pharmacy

lioresal baclofen

yasmin

sildenafil 20 mg mexico

brand viagra 50mg online

how much is cialis pills

price of sildenafil citrate

tadalafil 2.5 mg cost

real cialis online pharmacy

sildenafil 90mg

where can i buy cheap viagra online

diclofenac 30 mg

buy cheap viagra online without prescription

buy viagra uk pharmacy

medrol medicine

generic viagra 20 mg

cialis 80 mg

discount generic viagra canada

tadalafil 2.5 mg india

tadalafil generic usa

cheap viagra online in usa

online viagra in usa

ivermectin iv

cost of ivermectin

ivermectin 3 mg dose

plaquenil 200

gabapentin 204

erectafil 20 mg

cost of ivermectin

order sildenafil us

canadian prices for sildenafil

generic cialis price

no prescription cialis generic

australia viagra

stromectol pill

how to buy cialis in india

sildenafil usa

price of ivermectin liquid

allopurinol online canada

proscar uk online

how much is vermox

ivermectin 8000 mcg

stromectol cream

cost of viagra 100mg in australia

cheap viagra prices

robaxin 500 mg price

how to get viagra prescription online

cialis price usa

paxil delayed ejaculation

viagra 25

where can i buy cialis pills

where can i get sildenafil with no prescription

ivermectin covid

tadalafil buy canada

viagra cost

ecesoyser herseymanavgati eceboz57 ecedenizz hsaanbey farukby1

ventolin buy canada

best price for levitra 20 mg

generic for zanaflex

online pharmacy weight loss

thecanadianpharmacy

amoxil 800 mg

zoloft online no prescription

thyroid synthroid

trazodone no prescription uk

neurontin cap 300mg

where to buy sildalis

where buy indocin indomethacin

metformin without a prescriptions online

metformin 1000

buy accutane online canada pharmacy

tadacip cipla

combivent aer respimat

antabuse australia price

erectafil 20 for sale

aurogra 100 online

buy erythoromycin online

finasteride 1mg cost

clindamycin 600 mg tablets price

cost of synthroid generic

toradol 30 mg

nolvadex 20 mg price in india

buy zofran cheap

zoloft 125 mg

cleocin 150 mg cap

tetracycline antibiotic

order strattera online

augmentin 625 price in india

buy disulfiram online india

hydrochlorothiazide tablets

price of retin a 0.025

ivermectin 3 mg tabs

price of celebrex in canada

clonidine .1 mg

clonidine 01 mg

acyclovir cream price usa

how can i get viagra pills

erectafil 40

levitra viagra cialis

albendazole medication

sildenafil 20 mg tablet cost

cialis buy no prescription

modafinil 2020

viagra online usa cheap

dexamethasone 6mg

tadalafil 10mg cost

how can i get modafinil

neurontin from canada

generic metformin cost

can you buy synthroid over the counter

advair 500 50 mg

how to buy viagra online safely in india

allopurinol 400 mg daily

fildena 120 mg

buspirone 5 mg

compare zestril prices

buy antabuse 250 mg

sildenafil online prescription

buy zestoretic

viagra where to buy over the counter

generic cialis soft tabs suppliers

25 zoloft

buy valtrex uk

misoprostol 400 mg tablets

cipro xl

generic viagra online 100mg

cheap silagra

cialas

suhagra 50 mg buy online india

online cialis 5mg

sildenafil paypal

generic cialis fast delivery

viagra uk where to buy

online effexor prescription

orlistat generic

buy albuterol pills online

modafinil australia

singapore sildalis

dexamethasone 5 mg tablet

order strattera online

buy generic accutane

pharmacy online track order

celexa 200 mg

valtrex canadian pharmacy

buy malegra 200 mg

anafranil for anxiety

buy cialis otc

order strattera online

cost of prescription viagra

erectafil 40

levitra 20mg india